The pros and cons of treasury locks and forward-starting swaps as bond issuance jumps.

The crush of investment-grade issuers rushing to sell bonds as COVID-19 wreaks economic havoc has made pre-issuance hedging a relatively hot topic for many treasury teams.

- Chatham Financial, sponsor of NeuGroup’s Virtual FX Summit, helped members get a firmer grip on the various ways to manage interest rate risk—and the associated accounting implications—during the summit and a subsequent Zoom meeting.

Here are some of the key takeaways:

- Treasury locks are quite efficient as a short-term hedge (even intra-day), but can be less efficient when debt issuance is further out than three months, so it can be difficult to apply hedge accounting.

- They may be easier to explain to senior management than a forward-starting swap, but the market is also not as liquid nor as transparent.

- Another con: You’ll pay a “roll” premium if the tenor goes beyond the next treasury auction.

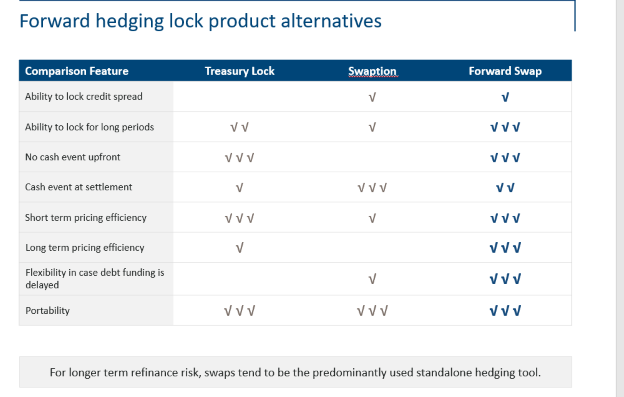

- Forward-starting swaps can be efficient as both a short-term and long-term hedge, but are predominantly used for longer-term refinance risk.

- While more liquid, forward-starting swaps also add an element of “basis risk” in the event that swap spreads compress over US treasuries, which in turn can add a layer of complexity when seeking senior management approval.

- Have a plan. Chatham Financial stressed that regardless of which option a company chooses, it’s important to have a plan in place including internal approvals that would permit the treasury team to execute hedges quickly if markets moved in a favorable direction. This sort of “readiness book” also helps prepare teams to strike while the capital markets are in their favor.

- Check out Chatham’s table below for more comparisons between treasury locks, forward-starting swaps and swaptions. And to dive deeper into the economic and accounting considerations, contact the experts.