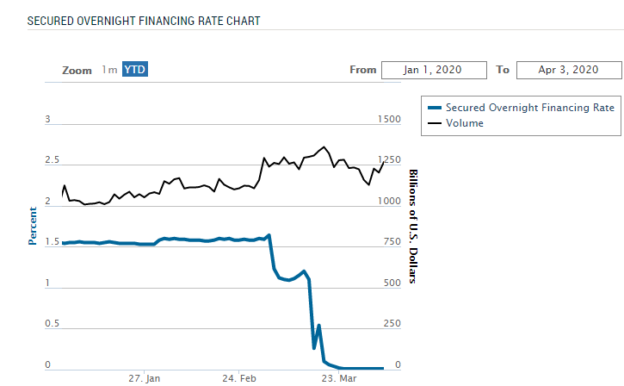

The volume of repo transactions underlying the calculation of SOFR has remained strong as the coronavirus disrupted other markets.

US regulators’ recommended Libor replacement has performed strongly through the volatility roller coaster powered by the coronavirus. In fact, the overnight repurchase agreement (repo) market used to calculate SOFR has increased in daily volume to more than $1.3 trillion.

- “With SOFR, you have good reason to be confident that it can always be calculated, and the rate you’re paying reflects actual transactions,” David Bowman, senior associate director at the Federal Reserve’s Board of Governors, told NeuGroup members at a recent virtual meeting. “Every market is challenged now, but the only one that really seems to be operating near standard capacity is the overnight treasury repo market.”

Libor extension unlikely. The futures exchanges’ move to SOFR discounting in October, anticipated to ramp up SOFR hedging, and other significant developments this year may be delayed—but only briefly.

- US regulators have little choice but to move forward with transitioning away from Libor, Mr. Bowman said, given banks’ unwillingness to submit their costs for wholesale, unsecured funding past 2021, when their agreement to continue submitting to Libor ends.

- New York State legislation designed to facilitate the transition from Libor has recently stalled as coronavirus took priority; but earlier “discussions were positive” and efforts should resume when the crisis calms, Mr. Bowman said. The bill would impact a wide range of corporate transactions, such as purchase agreements where the late payment fee is based on Libor, that typically lack language enabling the fallback to an alternative rate.

Corporate concerns linger. Mr. Bowman described efforts by the International Swaps and Derivatives Association and the Alternative Rates Reference Committee (ARRC) to develop SOFR contractual language and best practices, respectively, for derivative and cash transactions, to facilitate the transition. Corporates, however, are concerned that a forward-looking term SOFR has yet to emerge, and payments must be calculated in arrears.

- “We would want to see a full term structure, so we can base transactions off one-month and three-month SOFR,” said the assistant treasurer of a major pharmaceutical company, noting few corporates have issued SOFR-priced debt so far.

- Mr. Bowman said the ARRC is “committed to doing everything it can” to ensure the production of a forward-looking SOFR term rate, and it anticipates borrowers having a choice of solutions.

- He encouraged corporates to experiment with using SOFR calculated in arrears, noting that calculation needn’t occur shortly after the period ends but could be done five or 10 days before, giving more time to plan. “Don’t wait for a term rate—find out where you can use SOFR now,” Mr. Bowman added.

Calling all corporates. Mr. Bowman invited corporate finance executives to participate in his Friday afternoon office hours to discuss SOFR issues and to join ARRC committees and respond to its consultations. “Having you all help to shape the way this goes forward is vitally important,” he said.