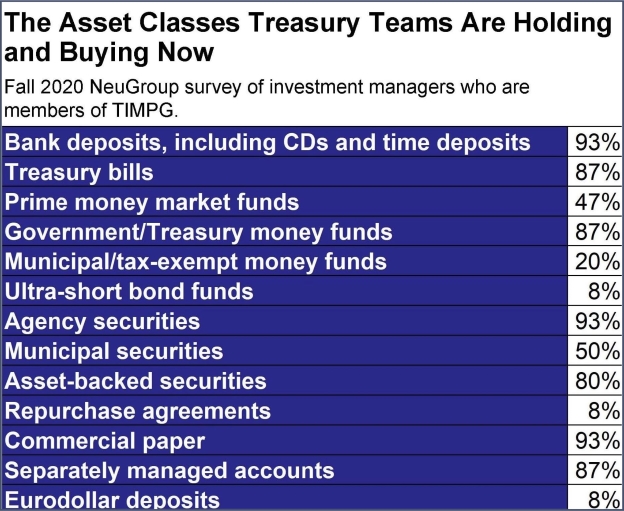

Treasury investment managers weigh options for finding returns in a low-rate environment.

Treasury investment managers looking to boost returns in the current low interest-rate environment discussed a range of options at a recent NeuGroup meeting sponsored by Morgan Stanley, including Treasury inflation-protected securities (TIPS) and municipal bonds.

- “We’re looking for alternative investment ideas to get attractive yield,” one member said. Her company is looking to return to investing overseas cash in low volatility net asset value (LVNAV) money market funds, an asset class it exited in March.

- Another investment manager said, “We are flooded with short-term cash, which is not great,” adding that her company is trying “to figure out how to deal with low rates.”

Why not reach for yield? In a discussion about credit risk, one member asked why investors who believe in the idea of a “Fed put” would not reach for yield during “a carry trade environment” where it “feels like fundamental research matters less and less.”

- Earlier, a Morgan Stanley portfolio manager said that it is “hard to think credit is wildly attractive here” given the contraction in spreads since March and that recovery “will mean tighter spreads than today.”

- In response to the member’s question, he agreed with the idea of a Fed backstop and said he has a hard time seeing a scenario where “spreads blow back out.”

- He said that if spreads widened from about 130 now to 145 to 150, “we would buy.” But he said that things may not go as the market expects and recommends investors be selective.

Tri-party repos, anyone? One manager is using tri-party repos, where a clearing bank acts as an intermediary and alleviates the administrative burden between two parties engaging in a repo. She said her company “disregards collateral” and proceeds if her team is “comfortable with the bank risk.”

- The company is also investing in three-to-five year financial and nonfinancial corporate bonds.

- It holds short-term government paper, including some Swiss and Japanese issues swapped back into dollars and yielding about 40 basis points.

- The manager is considering buying muni bonds, in part because she believes the timing is likely better now for investors than issuers.

Mulling munis. Other members asked about munis and one who invests in them offered to discuss offline the approach the company takes.

- The member who owns munis believes that another round of fiscal stimulus could benefit the asset class.

- A Morgan Stanley portfolio manager said munis may make sense for some corporates, depending on their tax situation and what happens to corporate tax rates after the election.

- A municipal strategist at Morgan Stanley estimates states will lose $180 billion and local governments $90 billion in revenue through mid-2021 because of the pandemic and recession.

- He said while there may be downgrades and different states will make different choices affecting credit ratings, “I don’t think default is the way to frame the discussion.”

TIPS debate. In response to one member who expressed interest in TIPS but has not figured out how they fit it to the company’s overall strategy, another member offered to put the first in touch with a “TIPS expert” who has done internal modelling with machine learning.

- A Morgan Stanley manager, who said TIPS had performed poorly in March and April, warned that “TIPS aren’t Treasuries” and that they have a “huge liquidity premium.” He said TIPS have a high correlation to high-quality corporates and “the extra yield doesn’t look that attractive.”