The abrupt stampede to safety in financial markets unleashed by COVID-19 in March 2020 created chaos and concern for investors, financial institutions and regulators. And it put extra scrutiny on the ability of digital solutions, systems and tools that underpin global trading, execution and settlement to serve and satisfy millions of financial professionals trying to do their jobs from home.

Chatham: Banks embedding zero-based floors in the fine-print on some floating debt.

With rates going negative around the world, banks are embedding zero-based floors into the floating-rate loans they provide, and while on the surface that seems like a plus, they can end up carrying a big price.

Chatham: Banks embedding zero-based floors in the fine-print on some floating debt.

With rates going negative around the world, banks are embedding zero-based floors into the floating-rate loans they provide, and while on the surface that seems like a plus, they can end up carrying a big price.

That was one of several insights on today’s uncertain financial markets that Kennett Square, PA-headquartered Chatham Financial provided in a recent market update titled. “Global uncertainty packs a local punch.”

Zero-based floors are valuable when interest rates are falling, because when they drop below zero, as they have across the Eurozone as well as in Japan, the borrower is obligated to pay the loan spread but zero interest on the floating rate component.

“On the surface, this seems like a pretty good deal. If rates go below zero, the borrower only pays its loan spread,” said Casey Irwin, a hedging consultant at Chatham, who conducted the recent webinar along with Amol Dhargalkar, managing director and head of Chatham’s global corporate sector.

Ms. Irwin noted that most banks “are not very upfront about” such floors effectively embedding the derivative into the company’s loan agreement, that the derivative is a sold floor, and that the floor can have a meaningful amount of value. “Unfortunately, clients discover the full value of these floors when they go to hedge these loans from floating to fixed,” Ms. Irwin said.

She added that in order to perfectly hedge a loan holding an embedded floor with a swap, the borrower must buy back the sold floor, and the cost of the floor is typically embedded back into the rate. Buying back the floor on a swap effectively locks in the interest rate at a static amount, Ms. Irwin said, adding that instead proceeding with the sale of the floor removes the loan’s ability to pay the borrower interest in the event the index resets below zero.

The borrower “is not only paying the agreed upon fixed strike of a vanilla swap to its counterparty, but it’s also going to owe the difference between zero percent and the [index] reset rate to the swap counterparty,” she said. “This is because its loan isn’t reflecting that negative interest rate.”

Buying back the sold floor is more expensive than selling the floor and proceeding with a straight vanilla swap, since it’s a one-sided market and most market participants are looking to buy back the floors. So is it worth it?

In an example provided by Chatham, a 10-year Euribor swap with a swap rate of 20 bps adds 40 bps to the rate when the borrower buys back the zero-based floor. Ms. Irwin noted that when the Euribor rate is a positive 1%, the only difference in the borrower’s net effective rate if it doesn’t buy back the floor—the vanilla swap scenario—is the additional cost of buying back the floor, or that 40 bps.

But if Euribor resets below zero, say at a negative 1%, the borrower will have to make an additional payment to the swap counterparty, resulting in an effective rate of 120 bps, or twice what it would have owed if it had bought back the floor. “So the mismatch between your hedge and your debt is actually creating interest-rate risk, because the more negative the index resets at, the higher your interest expense becomes,” she said.

In a brief case study, Mr. Dhargalkar noted a Chatham client that had entered into a term loan extension and was considering hedging it. The corporate client didn’t anticipate the amendment would in any way change the terms of the loan, but after showing the agreement to Chatham it became clear that the USD loan now contained a zero-based floor. The advisory firm discussed the various options with the client, and ultimately it was able to work with the client and the lending group to put in place a conditional floor that would only apply if the loan were not hedged.

“That had a huge impact on the transaction the client was looking to put in place; specifically, it saved several million dollars on the hedge from a structuring standpoint, and it also gave them a nice template for future dealings with their bank,” Mr. Dhargalkar said.”

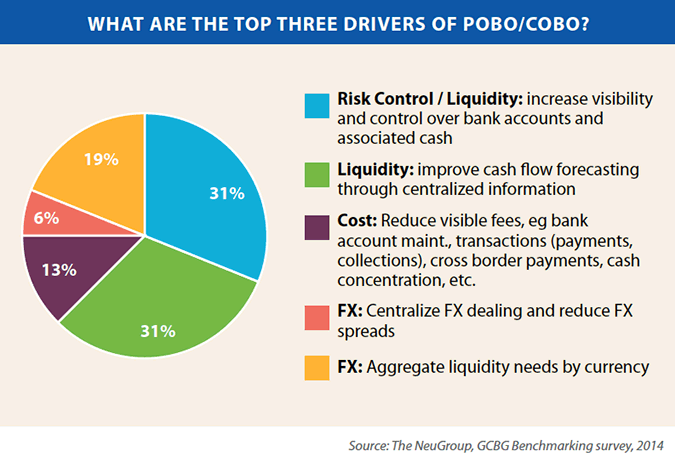

More companies are moving to streamline their payments and collections with on-behalf-of structures. Here are some lessons from the field.

Being a trailblazer is always nice but sometimes it pays to be the one who comes along next and learns from the trailblazer’s mistakes. And certainly, the more multifaceted the effort, the bigger the lessons learned. Such is the case with corporate payment and collections, part of the growing importance of supply-chain management and global cash management in general.

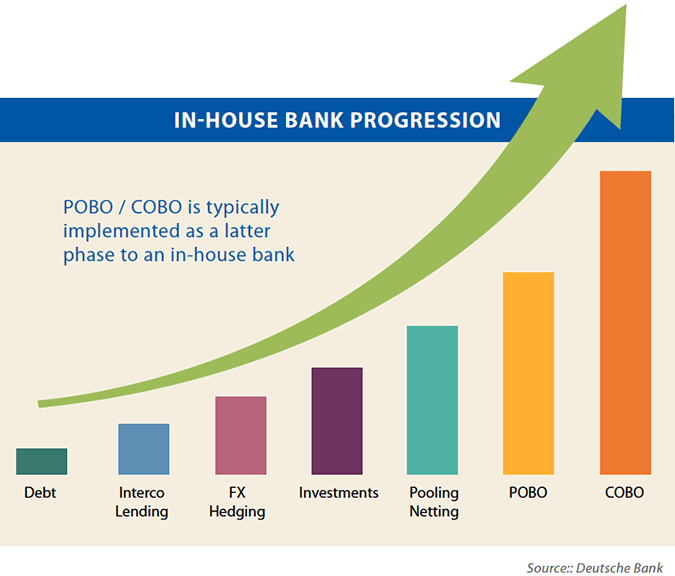

Corporates have long recognized the benefits of channeling payments and collections through a single legal entity via an on-behalf-of set up (POBO/COBO). They see reduced bank fees, simplified banking relationships, better operational efficiency and more control and visibility. Deutsche Bank has been one bank at the forefront of implementing on-behalf-of structures and has strengthened its product and advisory offerings in this area. iTreasurer asked Drew Arnold, Director, Trade Finance and Cash Management Corporates – Global Solutions Americas, Deutsche Bank, to explain some of the lessons learned in his experience implementing POBO/COBO structures. Mr. Arnold said that while all companies are different, there are some lessons that just about all companies can learn.

More companies are moving to streamline their payments and collections with on-behalf-of structures. Here are some lessons from the field.

(Editor’s Note—Original publication date: May 5, 2015)

Being a trailblazer is always nice but sometimes it pays to be the one who comes along next and learns from the trailblazer’s mistakes. And certainly, the more multifaceted the effort, the bigger the lessons learned. Such is the case with corporate payment and collections, part of the growing importance of supply-chain management and global cash management in general.

Corporates have long recognized the benefits of channeling payments and collections through a single legal entity via an on-behalf-of set up (POBO/COBO). They see reduced bank fees, simplified banking relationships, better operational efficiency and more control and visibility. Deutsche Bank has been one bank at the forefront of implementing on-behalf-of structures and has strengthened its product and advisory offerings in this area. iTreasurer asked Drew Arnold, Director, Trade Finance and Cash Management Corporates – Global Solutions Americas, Deutsche Bank, to explain some of the lessons learned in his experience implementing POBO/COBO structures. Mr. Arnold said that while all companies are different, there are some lessons that just about all companies can learn.

More Complex, More Benefit One lesson that Mr. Arnold has drawn from years of helping corporations navigate the path to both POBO and COBO structures is that companies often shy away from them because they think their organizations are too complex.

Very often, Mr. Arnold said, he hears from companies that say, “We’re too complex” or “We have too many operating companies.” But what’s ironic, he said, is that “the more complex [a company is] the greater benefit they can get from an on-behalf-of model; that complexity shouldn’t be a hurdle to doing an on-behalf-of model.”

It will mean performing more due diligence, however, Mr. Arnold acknowledged. But for doing that extra legwork companies can get “much greater benefit than someone who has a more simplified organization. In fact, he said, if a company has a very simplified legal entity structure, “there might not be any benefit to doing an on-behalf-of model, or the benefits are so low they don’t justify the costs of doing it.”

On the other hand, if it does seem too daunting or perhaps the resources aren’t available for a full-blown POBO/COBO campaign, another route is to take it one country or one subsidiary at a time. If one country has a lot of legal hoops to jump through, Mr. Arnold said, then companies should consider moving on to a different country that’s easier to navigate. As for subsidiaries, they can also be added piecemeal.

“You don’t have to include one hundred percent of your legal entities in a structure to be able to get the cost-benefit equation that makes sense for you,” Mr. Arnold said. “If a company can include 50 percent [of its subs] in a structure, and they’re going to see great cost savings and efficiencies by including that 50 percent, that alone may justify putting in an on-behalf-of model.”

And then over time if it makes sense to include other entities or if regulations or market practice change in the previously bypassed countries, they can be added as they make sense. “So one hundred percent inclusion of countries or legal entities is not a requirement to be able to build a business case that justifies going ahead with an on-behalf-of model,” Mr. Arnold said.

Worth the Effort Similarly, Mr. Arnold observed that many companies finish the POBO/COBO process and say that it was the toughest implementation they’ve ever been through. But, he added, no one who has gone through the set up ever regrets it.

“Many people say they were not aware of how long it would take,” Mr. Arnold added. They go on at length about all the difficulties, the challenges “not realizing how long it would take to put in service level agreements (SLA) between businesses or to define services or get the IT to work.” The challenges and work is definitely more than they expect, which is usually the case on any big project, Mr. Arnold said. “But then I always ask the question, ‘Knowing what you know now of what you had to go through to get where you are today, would you make the same decision?’ And they always say, ‘Absolutely.’”

This is certainly not something that one hears after many other large implementations, Mr. Arnold pointed out.

Welcome to Documentation One of the more cumbersome areas in the work load—and one that Mr. Arnold said companies underestimate—is documentation. When companies use banks for payments and collections or they open an account, the bank provides the documentation that the client reads, signs and sends back to the bank. In other words it lays out all the terms and conditions and other relevant items.

“But when you go to an on-behalf-of model [now], that legal entity no longer signs all of its bank documentation, so instead of getting documents from the bank you now get them from the in-house bank,” Mr. Arnold said. “And the complexity is that there is no documentation that exists; it has to be done from scratch—SLAs, fee schedules (i.e. transfer pricing) and whatever it may be, because there is this arm’s-length relationship between the in-house and the legal entity. It’s sort of out-insourcing.”

Companies now have to do all this documentation on their own and between themselves, which can take time for a company to create. On the bright side, however, once the documentation is established the work is much less, but at the beginning it can be very complicated and time-consuming.

And again, Mr. Arnold said, it can vary by country which is one of the reasons bank documentation is so complex in the first place. “It’s not because we love complex documentation it’s just because of regulatory challenges in countries, and so now with an on-behalf-of model, companies have to take care of this themselves.”

Laying the groundwork Like most big corporate projects, success depends a lot on the effort put in at the beginning. As Abe Lincoln famously said, “Give me six hours to chop down a tree and I will spend the first four sharpening the axe.” And so it should be in setting up a POBO/COBO structure. Getting the right team together and including all the parties from the outset will make the job easier to do and lessen the headaches along the way.

POBO/COBO “is highly complex and touches on many different parts of an organization,” Mr. Arnold said, “from treasury, to payables and collections teams, service centers, tax, legal, and both at the global and regional levels as well.”

Of those parts of the company, Mr. Arnold stresses it is the tax department that often can prove most critical. That’s because much of a corporate’s global strategy includes tax—if not actually built around tax issues. “All global corporates have developed their legal entity structure with a lot of input from tax,” he said, “So when moving to an on-behalf-of model you have to make sure that whatever you do will not in any way endanger or call into question the tax and legal-entity structure of the corporation.”

Mr. Arnold added that he’s seen several instances where treasury gets excited about doing a POBO/COBO project and after spending a considerable amount of time on it, brings it to the tax department where it gets shot down. “Tax takes the position that it has things set up in a certain way and you can’t go changing things,” he noted. “But if tax is involved early on in the discussion and it hears from a third party about what other companies have done… it becomes a lot easier.”

Mr. Arnold also stressed that POBO/COBO should not be sold as anything more than “an efficiency play.”

“The on-behalf-of model is not set up for any legal entity or tax optimization strategy,” Mr. Arnold said. “It’s purely an efficiency play: efficiency of making payments, collecting payments, managing the company’s liquidity, reporting at the entity level for the correct legal and tax reporting. So it’s efficiency; it’s cost savings.”

It is also a risk mitigation tool because you have greater visibility and greater centralized control, Mr. Arnold added, so you have reduced risk and a greater view into counterparty risk. “Once tax sees that, they’re more receptive to it.” Another consideration of laying the groundwork is to consider making it a long-range goal. “If you think you’re going to go to an on-behalf-of model anywhere in the near future, or within 5 years, you have to put in the building blocks.”

When opportunity knocks When is the best time to start the project? Mr. Arnold said it’s often best to embark on a POBO/ROBO project when there is another big project coming up or when there’s a bank change coming.

“If you’re going to go through some major bank changes due to acquisition or divestiture or because you’re moving businesses between relationship banks” then it can be good idea,” Mr. Arnold said. In an acquisition, for instance, treasury will have to open up new accounts, set up all new payment flows using the current set up in any case, so why not start up that new acquisition right away with an on-behalf-of model? “Why go through all the set up and then a year later… go to an on-behalf-of model? Why not combine them?”

Overall, what a company should do is clearly lay out the as-is structures and processes and then lay out the perfect-world scenario, or what Mr. Arnold calls “the blue sky to be.” And then break down that journey into phases. “Define the objectives very clearly in how they’re going to get there and put in that plan,” he said. “That plan might take multiple years to get to where they’re going.”

Strategic opportunity POBO/COBO structures are increasingly recognized as an efficient way to manage global cash. Although the initial set up of such a structure requires close coordination with tax and other partners, the ongoing benefits thereafter are well worth the initial legwork. That’s because it allows to treasurers to stop spending time on some of the mundane tactical responsibilities, allowing them to focus on the strategic, which ultimately adds more value to the company.

The silver lining in the new scrutiny of global transfer pricing is that treasury might finally escape from its cost center box.

The context here is the mess treasury is going to face with tax, cleaning up after the OECD BEPS Actions. The silver lining is that the new scrutiny of global transfer pricing might serve as justification for treasury to become a profit center, or at least set up treasury centers and in-house banks that get better compensated based on arm’s-length pricing for services rendered. Few external banks are offering a treasury services where they don’t earn a profit, unless the services are part of an overall “wallet” that is profitable–so why should an in-house bank not be generating profit when providing treasury services for group affiliates?

The silver lining in the new scrutiny of global transfer pricing is that treasury might finally escape from its cost center box.

(Editor’s Note—Original publication date: March 17, 2015)

The context here is the mess treasury faces with tax, cleaning up after the OECD BEPS Actions. The silver lining is that the new scrutiny of global transfer pricing might serve as justification for treasury to become a profit center, or at least set up treasury centers and in-house banks that get better compensated based on arm’s-length pricing for services rendered. Few external banks are offering a treasury services where they don’t earn a profit, unless the services are part of an overall “wallet” that is profitable–so why should an in-house bank not be generating profit when providing treasury services for group affiliates?

Arm’s length = profit To say that an arm’s-length price must have a profit margin in it, may be simplifying things a bit, but it helps get to the argument that treasurers should be overseeing profit centers in response to growing scrutiny on transfer pricing. They should make this argument because it helps them with the biggest issue they face: being starved for resources despite the huge value-added role treasury plays, because they have only relatively soft performance metrics to point to (compared to profits) when asked to cut costs.

Here is just one service where arm’s length pricing should generate a profit for treasury:

Centralized exposure management for affiliates. Paragraph 69 of the OECD Discussion Draft on BEPS Actions 8, 9 and 10 (on revisions to Chapter 1 of the Transfer Pricing Guidelines, including risk, recharacterisation and special measures) lays out the logic [bold is our emphasis]:

“Often a MNE group will centralise treasury functions with the result that the implementation of risk mitigation strategies relating to interest rate and currency risks are performed centrally in order to improve efficiency and effectiveness. It may be the case that the operating company reports in accordance with group policy a currency exposure, and the centralised treasury function organises a financial instrument that the operating company enters into. As a result, the centralised function can be seen as providing a service to the operating company, for which it should receive compensation on arm’s length terms. More difficult transfer pricing issues may arise, however, if the financial instrument is entered into by the centralised function or another group company, with the result that the positions are not matched within the same company, although the group position is protected. In such a case, an analysis of the conduct of the parties may suggest that the treasury function is not entering into speculative arrangements on its own account, but is taking steps to hedge the specific exposure of the operating company and has entered into the instrument essentially on behalf of the operating subsidiary. As a consequence the treasury company provides a service…”

Risk is an important component of proposed transfer pricing revisions, since the entity that assumes the risk (as does the entity that receives capital) should have a capability to add value with it (a new take on substance). This gets to transfer pricing rewarding the entity with the capability, not just one contracted to assume risk (or capital). [Note: There will be a public consultation on these transfer pricing matters on March 19-20 at the OECD Conference Centre in Paris.]

Treasury is often the function with the most capability to manage financial risk and thus arm’s-length transfer pricing should reward treasury for the services it provides in managing it, especially when it involves risk transfer between affiliates, but even risk management done on their behalf.

High value vs. low value-adding services In contrast to high value-adding risk management activities, there are low value-adding services that require arm’s length transfer pricing: Enough to reflect the service rendered, but not so much to shift profits unfairly by charging well in excess of their value add. The discussion draft for BEPS Action 10 (on Proposed Modifications to Chapter VII of the Transfer Pricing Guidelines Related to Low Value-Adding Intra-Group Services) suggests that financial transactions would fall outside the definition of low value-adding services, which may have transfer pricing determined on a more simplified cost-center basis.

However, one comment letter from bMoxie, a boutique Belgian professional services firm specializing in tax and transfer pricing, notes that financial transactions can be wide ranging, and thus not all treasury services would be high value:

“It is unclear what is meant with financial transactions. We tend to strictly define this is as the exchange of (financial) assets, and accordingly not be as broad as the full spectrum of financial services or services that relate to the financial position of companies. Indeed many multinational groups organize their financial services or treasury departments centrally to enable an efficient and effective service to the group members, which may include the execution of financial transactions, but also certain financial services. These services in turn may be fitting or not fitting the definition of low value-adding services. It is not uncommon that group treasury centers also provide auxiliary services that fit the examples of what is provided in paragraph 7.48 – i.e. that are merely of an accounting or administrative nature, and that do entail processing and managing of accounts receivable and account payable. In other words, the scope of a treasury department typically includes investment and funding activities, and may include other financial services that do require the assumption or control of substantial or significant risk, but may very well include services that could be considered low value-adding services, in the view of bMoxie.

Taking it one step further, even for instance in the light of a cash pool, that entails the exchange of assets, it may well be that the cash pool manager is only to be considered economically to be performing a pure clerical function when it contractually vis-à-vis the cash pool bank and the participants does not assume any risk, however in practice this would not unlikely be the case that the cash pool manager. We just wanted to make the point that even in the light of services auxiliary to financial transactions, there may be a certain division of activities amongst stakeholders that could lead one of the service providers rendering services that could technically qualify as low value-adding services.”

This sort of thinking will not get treasury out of its cost center box. It may also warrant more careful consideration going forward of what activities get put in a treasury center or in-house bank (e.g., payment and collection activities) vs. a shared services center, merely to keep the transfer pricing categorizations clean and the treasury-as-profit-center silver lining intact.

Understanding the standard document used to govern over-the-counter derivatives transactions.

Based on many discussions with practitioners in The NeuGroups’s peer groups here is a checklist of things to consider when implementing ISDAs.

One of the first considerations is whether it is worth bothering to set up an ISDA with every counterparty.

Understanding the standard document used to govern over-the-counter derivatives transactions.

Based on many discussions with practitioners in NeuGroup peer groups, here is a checklist of things to consider when implementing ISDA Master Agreements (ISDAs).

One of the first considerations is whether it is worth bothering to set up an ISDA with every counterparty.

Only value-add banks, please. With limited trading capacity to spread around—as well as treasury bandwidth—practitioners agreed that firms should focus on the banks that are able to add real value from an dealer standpoint. If they don’t, why waste time and energy on negotiating an ISDA?

Invest in a good ISDA template. Many treasurers also agreed that it is worth the money to pay a specialist attorney to create an ISDA template. This could be used as a starting point for negotiations with counterparties (or ending point, if firms are prepared to walk away if a bank does not accept the basic tenets of the template agreement).

Consensus has it that a template should be doable for anywhere from $50-100K in legal fees (fees should be coming down as more corporates turn to ISDAs and the more corporate-oriented clauses become part of law firms starter templates).

The need to involve internal counsel to cross-check these templates might raise the legal costs. Finally, while the first instinct might be to limit the ISDA to FX, it usually is more effective to consider the broader counterparty risk across asset classes, when preparing the template.

Choose your vintage. It pays to keep track of what the major differences are between the different “vintages” of ISDA templates (in practice, 1992 or 2002; see sidebar below), and be prepared to argue for the “preferred” one. Several members have mentioned how hard it is these days to have all their banks of the same vintage but that they have still been reasonably successful.

“We try to keep them standard,” said a treasury head whose company is “99 percent” on 2002 ISDAs; another has managed to keep all its banks to 1992 ISDAs. Marc A. Horwitz, an attorney formerly with Baker McKenzie (now with DLA Piper), noted: “For end users (corporates), we prefer 1992, particularly for FX trading.”

Banks are different. Each bank has a different risk tolerance and will focus on different areas, such as the definition of early termination, settlement, or credit committee concerns. Overall, members agree that non-US banks are harder than US banks, and Japanese banks, for example, are very conservative.

Don’t hesitate to stick to your guns. Treasury should not be afraid to play hardball with banks when negotiating their ISDAs, or if they are up for renewal. One way is the template approach; another is to flag the clauses that are a source for concern and stand firm regarding those. Check with senior management of course, but if you don’t like the terms a bank is offering, be prepared to say “no thanks” and walk away.

Also, just as banks have their pet peeves about what they consider important aspects of the ISDA to protect themselves, in the end, said one FX risk director, “you have to carve out various aspects of the [ISDA] contract you don’t like.”

Beware multiple-branch clauses. When specifying entities covered by the ISDA in the “schedule,” it is also important to be clear on the language on multiple branches, as this can help determine whether it’s better to book trades, for example, with the local Citi branch or Citi New York. One FX director noted that no matter which branch executes his company’s deals they are always “booked” with the London entity of the trading bank. One of his peers in the NeuGroup’s European Treasurers’ Peer Group (EuroTPG) agreed: “We insist on dealing with the main bank or branch, nobody else.”

Whether pricing is influenced by where the trade is executed is something to watch out for. A firm in the large-cap bracket with a bank in one region of the world may be covered by the medium-cap group in another, due to the relative size of its presence there. This could be true for one or several banks.

Banks should also not be allowed to book trades from branches located in jurisdictions which prohibit offshore FX transactions unless the ISDA is in the name of the onshore sub.

OTHER CRITICAL CONSIDERATIONS

Cross-default thresholds. A cross-default provision (under which all outstanding trades covered by the ISDA can be terminated if the counterparty defaults on third-party debt) can be elected in the ISDA schedule, but firms should consider whether to have it. When opting for the provision, it is important to set a threshold amount such that a cross default is not triggered unnecessarily by technical but not material events, and is not lower than existing credit agreements’ cross-default thresholds.

Termination settlements. In the 1992 ISDA form (see below), there are two methods for calculating an early termination settlement (triggered by “default” and “termination” events defined in the contract):

1) “Loss” (or “unpaid amounts”); and

2) “Market quotation.”

The former considers the amount that would make the counterparty whole on the trade. The latter requires four market quotes and the ultimate price is the average of the two middle quotes.

“Some corporates take strong views on which they prefer,” noted Mr. Horwitz, based on their experience with closeouts or what types of trade they plan to use most.

Market quotes work well for vanilla trades because it’s considered likely the trades will be priced fairly. The “loss” method works better for highly structured trades.

Confirmation supersedes ISDA. After a few corporate derivatives debacles in the 1990s, banks favor inserting a “non-reliance clause” into the 1992 ISDA (it is in the pre-printed 2002 form) in which the bank basically says “you (the company) know what you’re doing, so we’re not responsible.”

Very few corporates manage to negotiate out of the non-reliance clause. Because trade confirmations supersede ISDAs, those that don’t have the clause should take extra care that the clause does not get reinserted into the trade confirmations.

On the other hand (and this is another “score” for SWIFT), a corporate practitioner pointed out that using SWIFT confirmations helps in this regard as there is “not much room for sticking in additional terms or changes.”

THE TABLES ARE TURNED

While ISDAs may have been insisted on by banks in the past, it is now corporates that are scrutinizing them to ensure they are properly protected when banks look vulnerable. Firms, therefore, should take extra precautions to guard against events that may work against them at some future point in a trading relationship, when banks again look less vulnerable, starting with a mutually agreeable ISDA.

WINE AND ISDAS: VINTAGE MATTERS Should a firm opt for the 1992 or 2002 form of ISDA? The major differences between the two, said Baker McKenzie (now DLA Piper) attorney Marc. A. Horwitz, are:

Grace period for failure to pay. The grace period in the 1992 form is three business days, in the 2002, only one. For treasuries with limited bandwidth, three days’ grace can prevent mistakes and non-payments not due to credit default events from unduly punishing the firm or result in terminated trades.

Scope. The 2002 form includes a broader range of specified transactions, such as repos, reverse repos and securities loans. “For corporates, we generally prefer 1992; you don’t want an unexpected event in a non-ISDA trade to permit the bank to unwind this ISDA trade,” Mr. Horwitz said.

Force majeure. The 2002 form has a force majeure clause which governs termination of trades that are impossible to make payments on, after an eight business-day waiting period.

Right of set-off. The pre-printed 2002 form includes a set-off provision, which the 1992 form does not (it can be inserted).

Settlement. The 1992 form permits “loss” or “market quotation” as basis for the settlement price upon early termination. The 2002 form has a pre-determined method, a “hybrid” between the two, which doesn’t require four market quotes. There have been efforts within ISDA to migrate end users to the close-out amount, and while firms on the 1992 form can opt for this protocol, it “hasn’t taken that well with corporates,” Mr. Horwitz noted.

ELECTIVE EARLY TERMINATION As counterparty risk concerns remain pronounced both on the corporate and the bank side, corporates are reporting that banks are showing increasing interest in inserting an elective-termination clause into the ISDA (in the Other Provisions section).

For example, one bank has requested to insert it into a 1992 ISDA master with a corporate, which would allow either side to terminate a derivative six months after inception, and every six months thereafter.

The concern with such a clause is that the company is at risk of the bank terminating a long-term hedge by invoking this clause, leaving the company unhedged. This could cause unintended cash-flow consequences and, more importantly, problems with the hedge qualifying for hedge accounting treatment even at inception.

While the ISDA forms have specified “default” and “termination” events that are standard and bilateral, elective early termination clauses are not common, nor are they recommended in an ISDA governing a relationship, and that may cover a multitude of trades over a long period of time. Former Baker McKenzie (now DLA Piper) ISDA attorney Marc A. Horwitz pointed out that, absent a compelling regulatory or credit reason for such a clause, corporates should push back on banks trying to insert it.

A hedge, after all, is for protecting the corporation, not the bank, as a risk manager pointed out, and corporates already have a way to get out of hedges: by unwinding them; this, however, should be the firm’s decision, not the bank’s.

For many MNCs, an emphasis on effective management of working capital has translated into renewed urgency in rationalizing liquidity structures.

The tight credit market—combined with general economic weakness—has forced a strong focus on cash and liquidity management for both cash-rich and cash-poor companies.

As the ability to generate cash (or borrow it) has declined, MNCs report an increased need to have a clear view of their cash position globally. Visibility, however, is not enough. Treasurers also need effective techniques and procedures to manage their global liquidity. That task increases in complexity as a result of geographical spread, multiplicity of banking relationships, cross-currency flows and corporate structure issues (e.g., tax).

For many MNCs, an emphasis on effective management of working capital has translated into renewed urgency in rationalizing liquidity structures.

(Editor’s Note—Original publication date: June 16, 2003)

The tight credit market—combined with general economic weakness—has forced a strong focus on cash and liquidity management for both cash-rich and cash-poor companies.

As the ability to generate cash (or borrow it) has declined, MNCs report an increased need to have a clear view of their cash position globally. Visibility, however, is not enough. Treasurers also need effective techniques and procedures to manage their global liquidity. That task increases in complexity as a result of geographical spread, multiplicity of banking relationships, cross-currency flows and corporate structure issues (e.g., tax).

A consolidated view of cash

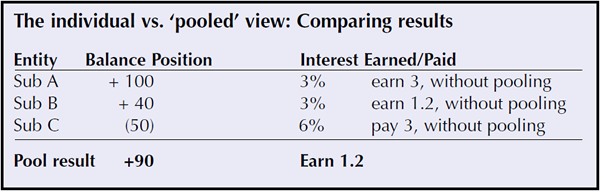

One of the most useful liquidity-management tools in the treasury toolbox is cash “pooling,” an arrangement whereby the credit/debit positions of different accounts are viewed from a single summary perspective.

This approach gives treasurers a chance to view cash on a regional and global basis, at the same time allowing affiliates to utilize their collective liquidity more effectively (i.e., instead of one subsidiary borrowing while the other is flush with cash).

Companies planning to centralize cash for multiple international subsidiaries have two basic options available:

• Zero balance accounts (ZBAs); or

• Notional cash pooling.

While both achieve the same ultimate objective, there are technical differences, which can then have significant organizational and tax consequences to either approach.

Zero-balance accounts (ZBAs)

ZBAs refer to linked accounts at the same bank and in the same currency and country. Funds are physically transferred in/out (zero-balanced) from subaccounts to a main account daily.

ZBAs: Key Aspects

The following are the key characteristics of a ZBA pooling arrangement:

• Same bank/same branch

• Same country

• Same currency

• Segregation of subaccounts which are then linked to a main account

• Completely automatic (bank), no manual transfers required

• Intercompany lending arrangements if separate legal entities participate, which means an arm’s-length interest rate must be assessed.

This primary account is usually held in the name of the Corporate Parent, Country or Area Headquarters/Holding Company or a Regional Treasury Center, such as a BCC, IFSC or OHQ.

If the subaccount holders are divisions of the same legal entity (such as branches, sales offices or plants), there are no tax issues. Indeed, often companies use ZBAs as a simple method to segregate different types of activities, such as receipts and disbursements, even if there is no regional or organizational segregation already in place.

However, if the subaccount holders are separate legal entities (i.e., subsidiaries), the funds movement into the main account constitutes an intercompany loan from the subsidiary to the main account holder and vice versa; this, in turn, generates some tax and accounting issues.

Audit trail and accounting. For example, documentation must be maintained for audit trail purposes and the main account holder (e.g., central treasury) must charge an “arm’s length” interest rate to the participating subsidiaries. Although banks provide separate statements for each subaccount, they will not typically do the accounting, manage the loan portfolio or assess/pay interest. (Some banks do run separate businesses which provide these services on an outsourced basis, usually out of Dublin.)

So unless this aspect of recordkeeping etc. is handled by a bank or third-party outsourced service, it must be done internally. Many treasury workstations and ERPs provide intracompany loan-management functionality as part of their core offerings. If the activity is at all substantial, spreadsheet solutions may not be sufficient (and certainly won’t provide the layer of automation of both interest allocation/payment and reporting that makes this cost effective).

Cost benefits. In-country ZBA arrangements are very common and have been a staple of managing US cash for years. Yet they are not universally possible. In certain countries, such as Korea, ZBAs may not be permissible at all, and in countries where there is an assessment of debit tax on transactions out of a bank account, such as Australia, a ZBA arrangement may end up being not cost effective.

For treasurers managing subsidiaries in multiple countries/currencies, the ZBA structure can be set up as an overlay, but funds must first be physically transferred from country A, B or C to the concentration location.

Two-tier approach. Often there is a daily pooling/ZBA in the originating country first, and then a sweep or manual transfer to the location of the main account, with less frequency. Thus the cross-border ZBA is usually a two-tiered structure. Weekly transfers are fairly standard. Daily transfers cannot be cost justified except with the very largest multinationals.

Therefore, in assessing the efficacy of overlay ZBA arrangements, a cost/benefit analysis is essential to establish the target level of cash required at the local level, and the frequency of transfer to the main account. Also overlay options may require opening additional in-country accounts, which can get expensive.

But perhaps the main drawback or limitation of ZBAs is that they’re only available on a single-currency basis. Thus, at the treasury level, there must be a main account for each separate currency.

Notional cash pooling

That’s where notional cash pooling enters the picture. With notional pooling, there is no physical movement of funds between accounts; rather, credit and debit interest are offset. Interest is paid/charged on the net balance position, but the legal/tax separation of separate subsidiaries owned by the same parent is maintained.

The initial (or direct) benefits of pooling come from the reduction of overdraft interest expense by centralizing the company’s liquidity position (see example in table below).

Legal hurdles. Notional pooling is great in theory. In practice, however, this pooling arrangement is not permitted in all countries. In these countries ZBA arrangements are used.

The big benefit to this arrangement, however, in the countries where it is most common, such as the UK, Netherlands and Belgium, is that there’s minimal or no withholding tax on interest earned. Often, too, (unlike physical pooling/ZBA arrangements) it’s not necessary to have a main or header account; the offset is simply among the participants. However, some countries (such as France) do require that there is a holding company in place.

The key advantage of notional pooling is that it allows for a multicurrency view of cash.

Notional: Key Aspects

The following are the key characteristics of a notional pooling arrangement:

• Same bank/ different branches

• Same country is most common

• Multicurrency pooling is extremely sensitive from a tax and accounting perspective—Spain can’t participate, for example due to local tax regulations

• Cross guarantees are required by the bank, regardless of the cash position of the participants

• Interest actually charged/paid to participants is optional—but may be advisable from a tax perspective.

However, in order to pay/charge interest on a single consolidated basis, the bank will use an interest rate differential to avoid currency conversion, similar to how a short-dated swap is handled. From a company’s perspective, this may ultimately affect the cost effectiveness of the arrangement. The company typically ends up paying forward points, thus reducing the interest-rate earned for a positive consolidated balance.

There is also a risk factor involved, as treasury is actually outsourcing this activity (to a bank). This means treasury may lose some control over the counterparties involved in the transaction.

Virtual pooling. In reality (or in virtual reality), treasury can achieve similar effects by using internal systems to execute the loans or interest offsets, and then generating the appropriate entries into the accounting system (i.e., an in-house bank). Also the rates achieved for investing excess cash would be higher. In fact, although a few large banks do offer multicurrency pooling, they are not entirely comfortable with it. (One of the very large banks simply decided not to offer notional pooling, only ZBAs are used; notional pooling was too fraught with difficulties).

In all cases, however, the bank will not act as a tax advisor, will insist on a sign-off from the company’s tax counsel and require cross guarantees between the participants. (That’s a hurdle for many MNCs.)

Loan by every other name. Pooling ostensibly gets around the issue of putting intercompany loans into place, because it is notional. However, it is a variant of a short-term intercompany loan arrangement, allowing a bank service to handle the periodic cash-reserve ups and downs of different entities.

If there were a permanent or long-term mismatch in liquidity, companies would more effectively use intercompany loans as the mechanisms. That’s why tax authorities will look carefully at pooling arrangements, and still may require some type of arm’s length interest depending on the amount and tenor of the offsets.

Also, if the company is always in an excess cash position, the concept of a notional offset makes no sense. And using a notional multicurrency pool as an investment vehicle is counterproductive, as the interest rate paid on the pool will be far lower than what individual currency pools will be able to achieve.

As a treasury management technique, cross border pooling is primarily used in Europe and to a more limited extent on Asia, where there are still regulatory issues that limit the participation of certain countries.

It is not used at all in Latin America (regionally) where there are significant regulatory issues and withholding tax restrictions on intercompany lending. Thus, the essential first step in evaluating any cross-border pooling arrangements is to focus on the management structure of the company and what tax implications may arise.