The abrupt stampede to safety in financial markets unleashed by COVID-19 in March 2020 created chaos and concern for investors, financial institutions and regulators. And it put extra scrutiny on the ability of digital solutions, systems and tools that underpin global trading, execution and settlement to serve and satisfy millions of financial professionals trying to do their jobs from home.

ServiceNow Treasurer Tim Muindi joins NeuGroup’s Strategic Finance Lab podcast to discuss his decision to do more to promote diversity and inclusionand how finance teams can do better at recruiting and retaining Black candidates.

In this episode of NeuGroup’s new Strategic Finance Lab podcast, ServiceNow treasurer Tim Muindi shares what Black History Month means to him, challenges he’s faced during the course of a 23-year career when he’s often been the only Black person in a company’s finance department and steps treasury teams can take to improve diversity and inclusion.

ServiceNow Treasurer Tim Muindi joins NeuGroup’s Strategic Finance Lab podcast to discuss his decision to do more to promote diversity and inclusionand how finance teams can do better at recruiting and retaining Black candidates.

In this episode of NeuGroup’s new Strategic Finance Lab podcast, ServiceNow treasurer Tim Muindi shares what Black History Month means to him, challenges he’s faced during the course of a 23-year career when he’s often been the only Black person in a company’s finance department and steps treasury teams can take to improve diversity and inclusion.

In the interview with NeuGroup Insights editor Antony Michels, Mr. Muindi also discusses his role in ServiceNow’s $100 million racial equity fund managed by RBC Global Asset Management that aims to boost homeownership, affordable housing and entrepreneurship in 10 Black communities where ServiceNow employees live and work.

Treasury must reinvent its role within finance or risk losing significant head count.

By Nilly Essaides

Technological advances and growth in the use of shared services centers (SSCs) are threatening to strip treasury of much of its operational activities. As automation supplants manual work and low-value activities migrate to SSCs, treasury may lose relevancy and staff. The tidal wave of digital transformation sweeping treasury means that smart automations like AI will replace current systems and the people who work with them.

An existential threat. At a recent NeuGroup meeting, Poly’s treasurer Jean Furter shared a radical view of the future of the function: “In three to five years, 90% of treasury staff will be gone,” he said. “Too many treasuries are still in the tactical mode. If that’s all they do, they risk being automated away.”

Treasury must reinvent its role within finance or risk losing significant head count.

By Nilly Essaides

Technological advances and growth in the use of shared services centers (SSCs) are threatening to strip treasury of much of its operational activities. As automation supplants manual work and low-value activities migrate to SSCs, treasury may lose relevancy and staff. The tidal wave of digital transformation sweeping treasury means that smart automations like AI will replace current systems and the people who work with them.

An existential threat. At a recent NeuGroup meeting, Poly’s treasurer Jean Furter shared a radical view of the future of the function: “In three to five years, 90% of treasury staff will be gone,” he said. “Too many treasuries are still in the tactical mode. If that’s all they do, they risk being automated away.”

Research conducted by The Hackett Group in 2020, meanwhile, projected that by 2025, 100% of the current work finance handles will be executed with 50% fewer FTEs. The caveat was that the overall workload will rise substantially as finance gets more involved with business and strategic activities.

While we may argue about the exact percentages, there’s no question treasury is exposed and it’s only a matter of time before the powerful trends reshaping the finance organization catch up with it.

The mass migration. Finance organizations are siphoning large chunks of time-consuming, low-value work away from core operations to highly digitized SSCs or GBS (global business services) organizations. By standardizing, automating and centralizing activities such as cash and general ledger accounting and credit and collections, finance is able to reduce process cost, while enabling end-to-end process management. Treasuries that own (or used to own) AP and AR are already feeling the squeeze. In fact, the majority of work handled by SSCs is finance related.

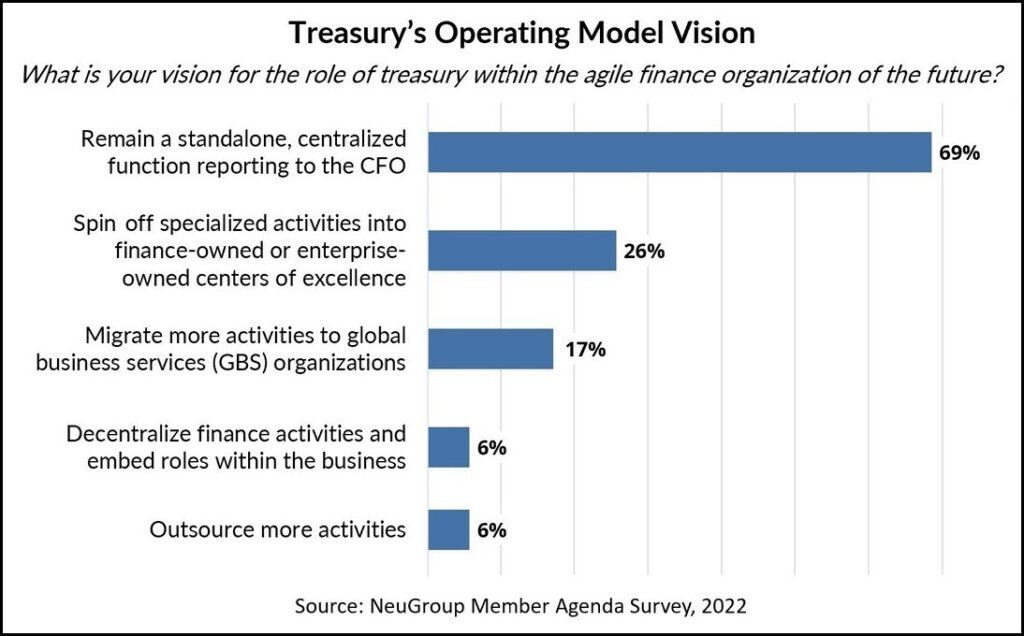

Choosing your destiny. That most treasury organizations have not embraced this vision of the future is evident in the results of the 2022 NeuGroup Members Agenda Survey (see chart above). Only 17% of respondents foresee transferring work to SSCs. If the nearly 70% who expect to see treasury persist as a standalone function are to be proven right, the function must take control of its destiny before leadership forces it to let go of a lot of operational activities.

The main reason we haven’t seen a more pronounced trend toward the migration of treasury’s tactical work is that the function is too small to find itself in management’s crosshairs. “Right now, companies’ primary motivation is to automate and centralize in order to reduce head count. Leadership is going after the biggest bang for the buck,” said the treasurer of one NeuGroup member company.

While there’s a distinction between SSC migration and pure automation (e.g., manual processes can also be transferred to low-cost locations), in practical terms, it does not matter whether a process is digitized and transferred to an SSC or automated and eliminated. In both cases, it no longer resides within treasury.

The danger of inertia. It can be easy to dismiss concerns about treasury’s slimmed-down future, in part because they are too threatening to contemplate, but mostly because most treasuries have not yet experienced precipitous declines in head count. On the contrary, many of our members are struggling to hire.

While automation will eliminate many treasury jobs, it does not mean treasuries will stop hiring. What will change is the profile of the people they hire. We already see this trend among our forward-looking members, as they try to recruit and develop staff with big-picture thinking and advanced digital skills.

Redefining treasury’s raison d’être. To be clear, we are not arguing that the treasury will disappear. We are saying that treasurers must figure out what the function will do when activities such as bank account management, cash positioning, short-term forecasting and reconciliation are automated and/or exported to an SSC. Whether treasury perseveres depends on how its leaders reposition the function’s role within the organization. “You have to position yourself as the source of insight and value,” Mr. Furter urges.

“Because of the specialized nature of treasury, for example, there will always be a capital markets group that needs the intellectual horsepower,” explained a respondent to the agenda survey. “Whereas on the [operations] side, that’s where we will see a deeper dive into automation and migration to SSCs; that’s where the head count will be reduced.”

Setting the right priorities. Treasuries have limited resources. If they spend too much time on perfecting ops processes, they won’t have the capacity to look higher, toward value creation and decision-support.

“You have to prioritize,” Mr. Furter said. Instead of producing a daily cash report, which rarely drives decisions or actions, do it weekly. “Just because real-time data is available, does not mean you need to spend weeks implementing it in your organization.”

While it remains important to reduce manual intervention through automation, it’s even more important to demonstrate to leadership how treasury can contribute real value through the design and execution of the capital structure, collaborating with the business to drive working capital, and managing financial risk, for example.

According to Mr. Furter, “These are elements that end up having a tangible impact on shareholder value.”

A temporary situation. For now, treasury cannot completely escape its operational duties and may have staff dedicated to these activities for some time. In this hybrid state, treasury is pushing operational excellence at the same time it’s pursuing a higher level of value creation. However, as fintechs introduce new technologies, such as blockchain and digital assets that aim to replace legacy financial market operations, treasury will find itself in a different position.

Above and beyond: Redesigning the operating model. The future of the treasury function is not just about shedding low-value tasks to create strategic capacity. It’s also about instigating a fundamental shift in how finance is organized, e.g., realigning treasury and FP&A activities. It’s incumbent upon treasurers to think strategically and lead high-level conversations about how to juxtapose different elements of finance.

FP&A focuses primarily on the income statement, yet it is still responsible for activities that are integral to the balance sheet and capital structure, such as long-term cash and debt forecasting.

Most FP&A leaders do not see their forecast within the context of the company’s leverage capacity and targets. It makes more sense to (1) organize around the balance sheet and the income statement; and (2) dismantle departmental barriers to integrate the management of both.

Cross-finance collaboration. Treasury leaders are on the right path. The majority of our survey respondents chose business partnering as their #1 objective for the year, by which they mean greater collaboration with other parts of finance.

“We continue to find ourselves touching lots of points in the finance organization, whether that’s tax or FP&A as well as legal; a lot of things that we decide upon have multiple impacts and stakeholders, e.g., creating trapped cash through the establishment of legal entities, or the impact of tax legislation on our ability to repatriate offshore cash,” one member said. Plus, “we’re partnering with legal on new share repurchase rules, and on cash forecasting with FP&A.”

Breaking the walls. Several trends will accelerate the dismantling of departmental silos. The rapid rise of digital assets and DeFi are forcing corporates to form cross functional task forces to study legal, tax, accounting, funding and payments implications. Plus, with surging inflation, treasury will have to work more closely with the business to determine how macroeconomic trends will impact the company’s ability to make good on its debt obligations or secure needed liquidity.

“There’s potential for more volatility going forward,” according to one survey respondent. So the partnership with FP&A is going to be very important.

Treasury of the future will look a lot different than it does today. Treasurers who continue to focus primarily on operational or tactical excellence may fail to establish their functions as valued partners in driving companies’ financial performance. Treasurers have a choice to make and ignoring the threats won’t make them go away.

Members compare notes and names as they outline the process for picking minority-owned brokerage firms.

Authenticity and shared values are what many corporates prioritize when selecting diversity firms for capital markets transactions. That takeaway emerged at a meeting of the NeuGroup for Diversity and Inclusion working group last month featuring three panelists from different companies.

“In identifying firms to work with, the most important aspect to us is the authenticity of the firm,” one panelist said. That means reviewing the diversity of the firm’s workforce, the advancement opportunities for minority employees, the actual jobs held by minorities and the path to ownership, he said.

Another said they assess the quality of a firm by finding out “who is in the organization, by layer, by type of diversity group.”

Members compare notes and names as they outline the process for picking minority-owned brokerage firms.

Authenticity and shared values are what many corporates prioritize when selecting diversity firms for capital markets transactions. That takeaway emerged at a meeting of the NeuGroup for Diversity and Inclusion working group last month featuring three panelists from different companies.

“In identifying firms to work with, the most important aspect to us is the authenticity of the firm,” one panelist said. That means reviewing the diversity of the firm’s workforce, the advancement opportunities for minority employees, the actual jobs held by minorities and the path to ownership, he said.

Another said they assess the quality of a firm by finding out “who is in the organization, by layer, by type of diversity group.”

One treasurer said his company seeks out firms that “have the same values as us,” something you can’t assume is always the case. “What we found was there are firms out there that do not share the same values,” he said.

Go beyond recommendations. Getting advice on which firms peers recommend is a starting point and members do share lists of preferred diversity banks and brokers. But one treasurer said the only way to know if a firm’s values match the corporate’s is through interviewing and observing.

“We had a few interviews where the owner didn’t show up,” he said. Or cases where most of the people who came to the meeting were white males, with perhaps just one member of the minority group the firm represented.

“If they’re telling you they’re a minority firm and minorities are just 26% of the people who work there, something’s just not right. That helps you narrow the field.”

Another area of inquiry: community relations. “We like to look at the community events they’re holding. What types of programs do they have for the folks who don’t have the opportunity, what are they doing?” he said.

A diversity firm’s capital markets capabilities, of course, are also a factor assessed by corporates.

Representation and communication. Members often select equal numbers of Black-owned, Hispanic-owned and veteran-owned firms, as well as those owned by women. One treasurer said the types of minority firms he picks correspond to his company’s affinity or employee resource groups, some of which are based on race.

One member asked the panelists how often they meet or communicate with the diversity firms on their rosters. One panelist meets with them once a year. Another said once a quarter if not more, saying frequent dialogue strengthens the relationship and establishes a long-term partnership with the diversity firm.

Forging that relationship is especially important to another panelist when the diversity firm is selected to be a joint-lead manager on a deal.

In those cases, he wants to get to know the people on the debt capital markets and syndicate teams. “We want to have a comfort level with who we’re working with because we’re asking them to play the same role as the other joint leads.”

A growing space. All of the panelists noted the rapid growth of the diversity firm space and expressed a desire to expand the number of firms that participate in their deals. Another treasurer whose company is a leader in using diversity firms for debt offerings told NeuGroup Insights:

“We believe in investing for growth in this space through differentiated and meaningful economics and meaningful opportunity when possible—which also allows new firms to get an opportunity, albeit at lower fees. Investing for growth to us is defined by number of employees at the firm (look for growth), capital base of firm (look for growth), and performance on transactions.”

Turning to banks, internal auditors and ERM teams may help treasury teams overcome a dearth of fraud data.

Payments fraud schemes hit 74% of companies in 2020, and two-thirds of treasury and finance professionals blame the pandemic for some of the increase in fraud at their companies, according to an AFP survey. Whatever the causes, the problem has made tools that can prevent scams more important than ever. But some treasury teams in need of those solutions are hitting a roadblock: Quantifying how much fraud the tools will prevent.

Members at a meeting of NeuGroup for Global Cash and Banking discussed how to build a business case for a new tool if the benefits of fraud prevention software would not be clear until it’s actually put to use. “A lot of the exercise is going to be theoretical,” one member said, which can be a hurdle when treasurers must convince traditionally data-focused leadership and IT teams to spare resources.

Some members recommended seeking answers by working with internal audit and risk management teams and the company’s bank group.

Turning to banks, internal auditors and ERM teams may help treasury teams overcome a dearth of fraud data.

Payments fraud schemes hit 74% of companies in 2020, and two-thirds of treasury and finance professionals blame the pandemic for some of the increase in fraud at their companies, according to an AFP survey. Whatever the causes, the problem has made tools that can prevent scams more important than ever. But some treasury teams in need of those solutions are hitting a roadblock: Quantifying how much fraud the tools will prevent.

Members at a meeting of NeuGroup for Global Cash and Banking discussed how to build a business case for a new tool if the benefits of fraud prevention software would not be clear until it’s actually put to use. “A lot of the exercise is going to be theoretical,” one member said, which can be a hurdle when treasurers must convince traditionally data-focused leadership and IT teams to spare resources.

Some members recommended seeking answers by working with internal audit and risk management teams and the company’s bank group.

The bottom line. One treasurer said her company had several recent “very near misses” with business email compromise schemes requiring her to tell banks to pull back the company’s funds. Now she’s seeking third-party fraud screening tools that analyze a company’s accounts and flag any suspicious payments. Deutsche Bank and TIS introduced one such tool last year.

One corporate cash manager found a solution in fraud screening functionality within the company’s payment factory, FIS Payment Hub – Quantum Edition. He said the tool screens and holds payments if there is a new beneficiary or if the instructions changed since the last payment. The entity that initiated the payment would then verify if a two-factor authentication process has been completed and reapprove the payment for release to the bank.

The functionality required additional resources, but the member said, “given the ever-increasing fraud landscape, I believe the investment in tools to detect fraud in our systems and training are important and worth the investment.”

Help from the outside and inside. Some members are seeking advice on building a case for tools like these, concerned that some fraud may currently be flying under the radar, undetected. Those who have implemented payments fraud prevention tools recommended seeking assistance from:

Banks. They have data on their clients’ previous fraud incidents, which can help establish a baseline for the level of fraud that could be prevented by a screening tool. One treasurer said he found success working with his bank to obtain fraud data from anonymous recaps of clients who have been scammed.

Internal audit teams. One member suggested working with the company’s audit team instead of attempting to quantify theoretical, undetected risk. Treasury can make note of previous issues or near-misses that may have been flagged in an audit report, which can be used to build out a more robust business case for fraud prevention tools. “Never waste a good audit,” the member said.

ERM teams. “If you have a fraud case that becomes a Wall Street Journal article or something, there’s a brand reputation connection, which tends to be flagged in the major ERM programs,” one member said. “If you can leverage what the ERM team have done, that can be helpful too.”

Cybersecurity teams. The member working with FIS to implement solutions in the company’s payment factory added that it’s worth getting to know your company’s cybersecurity team. “We’ve had a lot of success bringing them in from an advisory perspective to talk about risks to not using a payment factory, using portals outside of our IP filtering or a VPN and the risk that that entails,” he said. “Get to know them, work with them, and they can help you build a more robust business case.”

Editor’s note: NeuGroup’s online communities provide members a forum to pose questions and give answers. Talking Shop shares valuable insights from these exchanges, anonymously. Send us your responses: [email protected].

Member question: “Does anyone in the group discuss quarterly earnings with the rating agencies before the press release?”

Editor’s note: NeuGroup’s online communities provide members a forum to pose questions and give answers. Talking Shop shares valuable insights from these exchanges, anonymously. Send us your responses: [email protected].

Member question: “Does anyone in the group discuss quarterly earnings with the rating agencies before the press release?”

Peer answer 1: “If there is news that we believe they should hear in advance of the earnings announcement, then we do meet with them in advance.”

Peer answer 2: “We haven’t been asked to discuss earnings right before press releases. However, a rating agency asked us to provide an updated cash flow forecast/debt paydown in a blackout window, and we complied with the request.”

Peer answer 3: “We verbally discuss key aspects of the results in advance if we expect them to take an action post earnings. We don’t share any presentation materials until after the earnings.”

Peer answer 4: “We had talked to them before earnings releases. We recently changed and now do it after earnings updates. They have not reacted negatively so far.”

Peer answer 5: “We would share information prior to the earnings release if we felt it was significant enough to impact our credit.”

NeuGroup Insights reached out to Jonathan Richman, a partner at law firm Proskauer, for his perspective on potential legal issues that may stem from disclosing information with rating agencies in advance of earnings.

“The big concern is Regulation FD, which prohibits advance disclosure of material nonpublic information (MNPI),” he said.

“However, an issuer can disclose MNPI to a rating agency before public disclosure if the rating agency has agreed to keep the information confidential and not use it before it has been disclosed to the market in general.”

Advice and insights on how corporates can better recruit Black candidates and support their career advancement.

Finance leaders and hiring managers committed to diversity and inclusion (D&I) and increasing the number of Black people on treasury and other teams reporting to CFOs need to embrace new ways to recruit and hire Black candidates while creating a corporate culture that welcomes Black employees, encourages them to stay and supports their advancement.

That’s among the key takeaways from comments by finance professionals speaking in recent NeuGroup meetings and during interviews marking Black History Month. Another important point: achieving D&I goals requires active engagement and consistent attention.

Advice and insights on how corporates can better recruit Black candidates and support their career advancement.

Finance leaders and hiring managers committed to diversity and inclusion (D&I) and increasing the number of Black people on treasury and other teams reporting to CFOs need to embrace new ways to recruit and hire Black candidates while creating a corporate culture that welcomes Black employees, encourages them to stay and supports their advancement.

That’s among the key takeaways from comments by finance professionals speaking in recent NeuGroup meetings and during interviews marking Black History Month. Another important point: achieving D&I goals requires active engagement and consistent attention.

“You really have to make an effort to hire, retain and grow diverse talent,” said one member who is actively recruiting Black candidates. “I think there’s an idea of, ‘oh, we will just hire more,’ and everyone takes their eyes off it and expects to see them 20 years later in an executive meeting. Actually, it’s about that entire process and not taking your hands off of it.”

HBCUs and beyond. Tim Muindi, treasurer of ServiceNow, said in an interview that finance leaders who say they’re struggling to find more Black candidates “are probably not looking in the right places. That’s usually the biggest hurdle. I start by asking, ‘where are you looking?’”

He added, “In most cases, you have to go meet them where they are. For me, being in the Bay Area, we want to add more Black professionals to finance, our eyes have to be wide open for potential opportunities, whether it’s in Detroit, Atlanta or wherever the case might be.”

As part of that approach, Mr. Muindi said ServiceNow has expanded beyond recruiting at a few schools to reaching out to more historically Black colleges and universities (HBCUs) and schools located in areas with larger Black populations.

Summa Simmons, director of treasury at Victoria’s Secret & Co., told NeuGroup Insights that large HBCUs attract heavy recruitment from the Big Four accounting firms, but “there are tons of budding accountants and finance professionals that don’t necessarily want to go to the Big Four and are open to other career tracks beyond public accounting.” She also recommends talent acquisition/recruiters look beyond the larger HBCUs, saying, “there are tons of great HBCUs, sometimes local to the city companies are hiring in.”

The treasurer who is actively recruiting Black candidates said she’s had great experiences working with HBCUs. “You’re playing the long game, you’re investing in them when they’re really young and growing through the organization,” she said. “You can’t hire someone at the director level with this path, but it’s been tremendous.”

Connecting with candidates. A number of members recommend working with the National Association of Black Accountants (NABA) and The Robert Toigo Foundation, industry groups that can help connect companies directly to potential candidates through job postings, mentorship and in-person job fairs and conferences.

For in-person or virtual job fair events, Ms. Simmons says it is important to have diverse recruiting teams. “Make sure you bring employees and associates that look like the people you want to recruit—I think that’s the biggest piece of it,” she said. “Find the diverse talent in the finance organization and get them on a rotational schedule supporting recruiting initiatives so your prospective candidates can have candid conversations.”

In recruiting Black candidates, the presence of people doing interviews who look like a candidate is “huge,” Mr. Muindi said. “The fact they can see somebody who looks like them in that role, it gives them a sense of belonging. They feel like, ‘This is a place I can go, start my career, grow my career and potentially even get to those senior levels.’ That really helps with that connection.”

Black and African American candidates can’t always tell if a company’s commitment to diversity is real, Ms. Simmons said. So there are a number of questions potential employees may ask to distinguish lip service from true commitment:

Is the appraisal system designed for employees to get direct and helpful feedback?

Is there a development plan that leaders work on with employees?

If employees express interest in promotions but don’t get them, are they getting meaningful feedback?

If the company is successful in attracting diverse talent, does it have a robust and inclusive initiative to help retain that talent?

When diverse candidates come in, are there mentorship opportunities?

Mentors, sponsors and allies. Mr. Muindi said that while he has had good experiences with mentors throughout his 23-year finance career, he has found sponsorship in short supply at more senior levels, defining a sponsor as somebody who will recommend someone else for opportunities—an essential part of rising through executive ranks.

“I think it’s challenging across the board, but I think it’s more challenging when you are a minority. In most cases, they don’t have anybody that they relate to on those higher levels and have a relationship with, so it becomes more difficult to find that sponsor,” he said.

Ms. Simmons, who leads Victoria’s Secret & Co.’s Black and African American inclusion resource group, said that it is also important to have allies at a company to foster a culture of true commitment to diversity and inclusion. To hear her thoughts on the importance of allyship, as well as what Black History Month means to her, please watch this interview excerpt.

NeuGroup members in charge of DC plans discuss implications for ESG investment options and record-keeping.

NeuGroup members who oversee corporate 401(k) plans are weighing the fiduciary implications of a recent Supreme Court ruling in favor of employees of Northwestern University who claimed their defined contribution (DC) plan charged excessive fees and offered confusing investment options. The unanimous decision said a lower court erred in ruling that because Northwestern’s plan included diverse investments, the workers could not sue over fees tied to some of the options.

At a recent meeting of NeuGroup for Pensions and Benefits sponsored by Insight Investment, members mentioned the Northwestern case as a possible factor in deciding whether to offer ESG investment options in their DC plans, and as additional motivation to do new request for proposals (RFPs) for record-keepers.

NeuGroup members in charge of DC plans discuss implications for ESG investment options and record-keeping.

NeuGroup members who oversee corporate 401(k) plans are weighing the fiduciary implications of a recent Supreme Court ruling in favor of employees of Northwestern University who claimed their defined contribution (DC) plan charged excessive fees and offered confusing investment options. The unanimous decision said a lower court erred in ruling that because Northwestern’s plan included diverse investments, the workers could not sue over fees tied to some of the options.

At a recent meeting of NeuGroup for Pensions and Benefits sponsored by Insight Investment, members mentioned the Northwestern case as a possible factor in deciding whether to offer ESG investment options in their DC plans, and as additional motivation to do new request for proposals (RFPs) for record-keepers.

Members also discussed another area where fiduciary concerns have been constraining the interest of some companies to innovate: offering so-called retirement income solutions within 401(k) plans.

The litigation explosion. One member doing an RFP for his company’s pension and 401(k) plans said the Northwestern case and others underscore the need to “make sure our governance is very tight—all you have to do is open the news and see so many litigations going on over plan administration and record-keeper fees.”

More than 150 proposed class actions challenging retirement plan fees have been filed over the past two years, according to Bloomberg Law. The majority remain active, with about 20 cases put on pause while the Supreme Court deliberated the Northwestern case, Bloomberg reported.

Another member said the Northwestern decision also raises “interesting” questions about ESG investments companies might offer in DC plans that may not provide returns as high as other options or may have higher expense ratios. “As a fiduciary, do we violate some of those requirements, especially when we look at the Northwestern judgment?” he asked.

Roger Heine, senior executive advisor at NeuGroup, noted that a recent Department of Labor proposed rule attempting to provide plan providers a legal safe harbor to offer ESG-oriented funds seemed to fall short. The ruling implies that ESG funds are okay only because they offer superior long-term returns and hence meet existing fiduciary standards. “But what happens if a company offers employees an ESG fund that subsequently underperforms the market?” he asked.

Retirement income solutions: no rush. Discussion at the recent meeting returned to a topic that has also raised regulatory concerns for members: offering retirement income solutions including annuities within DC plans. In the past, many companies feared that if the insurance company providing an annuity failed, the company might be liable.

The SECURE Act, passed at the end of 2019, included provisions to create an ERISA fiduciary safe harbor in case the annuity carrier did in fact fail. Nonetheless, nearly three-quarters of members surveyed last June said that the act did not make them comfortable enough to offer annuities in their DC plans.

Another member said her company is not looking to put something in place in the next 12 months and is doing more of a product study to “get to a place where we might be able to offer something to participants at some point in the future.”

She added, “There have been a lot of different products hitting the market over the last couple years. There are some different approaches out there now in terms of what’s in plan, what’s out of plan, how the products are structured.”

A third member, returning to the theme of record-keeping, said, “Even though I don’t think there are a lot of great retirement income options available right now, we’re at least having conversations with our current and prospective record-keepers so we would be prepared [to offer] retirement income or maybe a retirement tier.”

Communication and inflation. Mr. Heine of NeuGroupnoted that members also have indicated that adopting a retirement income solution would be a major undertaking including employee communications exercises, while limited corporate DC staffs are already occupied just making sure current, simpler offering of funds remain appropriate and at competitive costs.

“Some members have said that other specialized 401(k) offerings such as ESG-oriented funds and managed accounts have seen surprisingly little uptake from their employees, so the effort and cost have gone wasted,” he said.

“Perhaps companies sense this is an inopportune time to offer annuity products to their employees,” he added. “Fixed annuities are highly vulnerable to inflation and their pricing now is calculated off of today’s very low interest rates, which remain well below inflation. Perhaps, if eventually rates rise enough and inflation abates, interest in expanding into retirement income products will pick up.”

HighRadius helps one company with thousands of projects and a complex revenue stream better forecast cash.

A new tool to improve cash forecasting can be a tough sell to management, given the intangible returns. It becomes easier, however, if the solution improves accuracy by more than 50%, and even easier if the vendor contractually agrees to achieve a certain level of improvement or discontinue the relationship—no strings attached.

“It’s very hard to put a dollar amount on the positive impact of a cash forecast,” the treasurer of a company that had implemented a cash forecasting platform told members of NeuGroup for Large-Cap Assistant Treasurers.

“Our president once said to me, ‘So who cares if you’re wrong?’ But if that happens, he’s not happy about it.”

HighRadius helps one company with thousands of projects and a complex revenue stream better forecast cash.

A new tool to improve cash forecasting can be a tough sell to management, given the intangible returns. It becomes easier, however, if the solution improves accuracy by more than 50%, and even easier if the vendor contractually agrees to achieve a certain level of improvement or discontinue the relationship—no strings attached.

“It’s very hard to put a dollar amount on the positive impact of a cash forecast,” the treasurer of a company that had implemented a cash forecasting platform told members of NeuGroup for Large-Cap Assistant Treasurers.

“Our president once said to me, ‘So who cares if you’re wrong?’ But if that happens, he’s not happy about it.”

The treasurer detailed his team’s journey from Excel spreadsheets to HighRadius’ artificial intelligence driven platform. He said its use, limited to 2021, had performed well above expectations.

Remarkable results. The treasurer said the company had tracked its cash forecasting accuracy for years, and the new platform improved the three-month forecast net accuracy by 59% and the six-month forecast by 80%.

Net accuracy of the three-month forecast rose to 95% and the six-month forecast to 97%.

“What’s remarkable is that as you go out further it’s even more accurate,” he said. The company uses HighRadius for cash forecasts over the first six months, and for longer forecasts tacks on its traditional, top-down approach.

The challenge. The company concurrently runs more than 1,000 projects, each with numerous subcontractors that are paid at completion.

Each project essentially has its own “mini P&L.” If the cash performance of one out of five projects for one client wanes, it requires a deep dive to the invoice level to arrive at an accurate cash forecast.

“But treasury just didn’t have the resources to do that, so we had to find an automated solution,” he said.

Understanding the data. The company’s treasury team spent several months working with HighRadius to understand the data science and explain the company’s different cash flow categories and types of data, providing HighRadius with three years of invoice-level data.

In one instance, treasury initially sent over customer payment files, and HighRadius requested more detailed data at the project level.

“That was impressive stuff,” the treasurer said. “HighRadius figured out what data they needed from us and at what level; again, the process of really understanding the data.”

Applying AI. The company sends scheduled items such as payroll and debt service to the HighRadius platform, and its accounts payable (AP) and accounts receivable systems (AR) running data weekly automatically send that project level information. Meanwhile, the company’s banks send relevant data every 15 minutes.

AP and AR are the two components that are hardest to forecast, he said, and HighRadius’ technology determines the best artificial intelligence (AI) algorithm to use for each project.

“Now instead of a top-down forecast, you have the bottoms-up forecast you would do if you had the resources to do it yourself,” the treasurer said.

Cash management. After cash forecasting, the company implemented HighRadius’ cash management screen, enabling treasury to see current cash in the bank as well as investment values.

The treasurer said that cash management and forecasting are combined on one screen, providing holistic view of the company’s cash position.

“I know how much cash I have in the bank and based on my forecast I can see where I am at the end of the week, and then I can drill down and look a t that daily,” he said, adding that the weekly forecast is especially helpful, for example, on payroll weeks when the firms may have to borrower from its revolver.

ServiceNow treasurer Tim Muindi reviews how a racial equity fund is making a difference.

A year ago during Black History Month, ServiceNow’s Tim Muindi—a senior treasury director at the time—shared with other NeuGroup members his role in launching a $100 million racial equity fund managed by RBC Global Asset Management. The fund’s objectives centered on boosting homeownership, affordable housing and entrepreneurship in 10 Black communities where ServiceNow employees live and work.

A year later, Mr. Muindi—now the software company’s treasurer—sat down for a virtual interview with NeuGroup Insights to review the deployment of the capital and the impact of the investment. “What I’m really proud of is the fact that we’ve been able to really impact low- and moderate-income [populations],” he said. “When we look at the allocation of our fund, it was done to target a demographic that is really marginalized.”

Mr. Muindi also discussed what Black History Month means to him, challenges he’s faced during the course of a 23-year career when he’s often been the only Black person in a company’s finance department, and steps treasury teams can take to improve diversity and inclusion. Please watch a video interview on those topics below.

ServiceNow treasurer Tim Muindi reviews how a racial equity fund is making a difference.

A year ago during Black History Month, ServiceNow’s Tim Muindi—a senior treasury director at the time—shared with other NeuGroup members his role in launching a $100 million racial equity fund managed by RBC Global Asset Management. The fund’s objectives centered on boosting homeownership, affordable housing and entrepreneurship in 10 Black communities where ServiceNow employees live and work.

A year later, Mr. Muindi—now the software company’s treasurer—sat down for a virtual interview with NeuGroup Insights to review the deployment of the capital and the impact of the investment. “What I’m really proud of is the fact that we’ve been able to really impact low- and moderate-income [populations],” he said. “When we look at the allocation of our fund, it was done to target a demographic that is really marginalized.”

Mr. Muindi also discussed what Black History Month means to him, challenges he’s faced during the course of a 23-year career when he’s often been the only Black person in a company’s finance department, and steps treasury teams can take to improve diversity and inclusion. Please watch a video interview on those topics below.

Numbers and people. ServiceNow provided all $100 million of the racial equity fund upfront and RBC invested it throughout the year, completing the deployment by year-end 2021, Mr. Muindi said. Where it went:

More than 90% funded home ownership, supporting about 360 mortgages. Although a lot of information about mortgage recipients is undisclosed, RBC’s experience and use of census data helped pinpoint communities with large Black populations, Mr. Muindi said.

In the end, 97% of the borrowers benefitting from the fund earned less than 80% of the median income in the area where they lived. Mr. Muindi said the lack of more detailed data about end beneficiaries is not a deterrent to funding mortgages, adding, “We’re making a difference in the community.”

Half of the remainder funded various improvements and enhancements in about 1,100 rental units. The vast majority of the affordable housing funds went to a pair of properties in Chicago where 99% of the population is Black, with many women-led households making less than $9,000 per year, Mr. Muindi said.

The money went toward rehabbing the properties, “making sure that they have upgraded appliances, paint jobs, also building playgrounds where the kids can go and play so it feels more like a community rather than just a place of dwelling,” he said. “That was really a great outcome for us to see that.”

About 15 businesses in 13 different industries received the other half of the remaining funds. The recipients of the entrepreneurship funds included a small construction firm in Florida that Mr. Muindi said provides employment to about 70% of the area’s Black population.

Returns and the road ahead. Mr. Muindi said ServiceNow earns a return on the fund, but that’s a secondary objective to having an impact in Black communities. “Any returns we get we’re putting right back in the fund to continue building these sustainable opportunities in these communities.”

Looking ahead, ServiceNow will now evaluate its options, including looking for investment opportunities beyond the racial equity fund. “There’s a lot of room out there for us to continue making an impact, so we’ll be very thoughtful about how we deploy any additional investments,” Mr. Muindi said.

Speaking broadly of finance teams, Mr. Muindi said, “We have to get off the sidelines. And that’s been a big theme for me. If you want to drive change you have to get off the sidelines, get on the field. It’s not perfect, we’ll make mistakes. But we’ll be trying and then we’ll learn through that.”

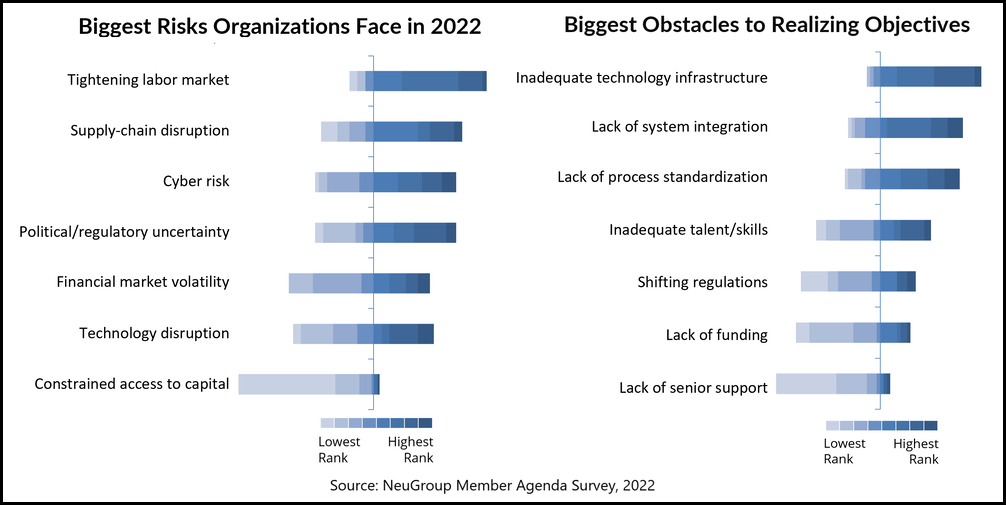

The labor market is treasury’s top risk, but aligning talent with business needs is its No. 4 priority. Is that a problem?

It may not shock anyone that treasurers say a tightening labor market is the top risk they face this year (see chart), according to the January 2022 NeuGroup Member Agenda Survey. More intriguing: the same treasurers rank aligning the skills of their team members with business needs just fourth among their top objectives. No. 1 on that list: collaborating with business partners to drive performance.

The labor market is treasury’s top risk, but aligning talent with business needs is its No. 4 priority. Is that a problem?

It may not shock anyone that treasurers say a tightening labor market is the top risk they face this year (see chart), according to the January 2022 NeuGroup Member Agenda Survey. More intriguing: the same treasurers rank aligning the skills of their team members with business needs just fourth among their top objectives. No. 1 on that list: collaborating with business partners to drive performance.

Another data point to consider in assessing treasury’s view of the talent challenge: inadequate skills and talent also ranked fourth on respondents’ list of biggest obstacles to achieving their objectives; inadequate technology infrastructure ranked No.1 (see chart).

“There may be a disconnect between labor market risks and the urgency of ensuring that treasury teams have the right people to achieve their aggressive goals,” said Nilly Essaides, NeuGroup’s managing director of Groups, Research and Insight. “Finance, as it has in the past, may be underestimating the importance of talent development to its success.”

Treasury’s ability to transform into a more strategic business partner, Ms. Essaides added, depends on whether teams possess the right talent and skill sets to talk to the business in its language, communicate effectively, think critically, provide insights and tell stories.

The tech obstacle. The success of treasury’s ability to add strategic value depends not only on talent management, but how soon it overcomes the obstacles of insufficient technology infrastructure and a lack of system integration (No. 2) and achieves its No. 3 top priority, accelerating digital transformation.

For example, process automation and integration, achieved through building a stronger tech stack, is critical for creating capacity to address higher-value tasks and improve accuracy and control, Ms. Essaides said. And system integration allows treasury to “reduce friction in the flow of information and data, saving time and improving treasury’s ability to curate relevant data to support decision-making.”

It’s also important to recognize that adopting better technology does not necessarily mean the loss of people. “The thing with automation in general is that it’s not just about replacing human activities,” Ms. Essaides said.

“Some of the simple first-level automations are exactly about that, but to be really transformational, technology needs to augment what people do in order to support decisions, through advanced analytics and machine learning, for example.”

Editor’s note: NeuGroup’s online communities provide members a forum to pose questions and give answers. Talking Shop shares valuable insights from these exchanges, anonymously. This exchange is from NeuGroup for Growth-Tech Treasurers.

Member questions: “I am working on optimal target capital structure (debt/equity mix) analysis and framework. Any ideas on approach/model?

“I’m also working on creating a capital allocation policy and framework. Any sample allocation policies and framework approach or model ideas would be great.”

Editor’s note: NeuGroup’s online communities provide members a forum to pose questions and give answers. Talking Shop shares valuable insights from these exchanges, anonymously. This exchange is from NeuGroup for Growth-Tech Treasurers.

Member questions: “I am working on optimal target capital structure (debt/equity mix) analysis and framework. Any ideas on approach/model?

“I’m also working on creating a capital allocation policy and framework. Any sample allocation policies and framework approach or model ideas would be great.”

Peer answer 1: “There are several decision points to consider for capital structure:

Fixed vs. floating interest rates: consider your risk tolerance for fluctuating rates.

Type of instrument: term loan A vs. term loan B; secured vs. unsecured; bonds vs. notes, considering credit rating and the desire to have the flexibility to prepay vs. having more permanent capital.

Revolver needs: asset based vs. cash flow based, driven by the rating, amount of liquid working capital available, stability of cash flows, working capital cycle needs and seasonality. Size based on stress testing, availability of internal cash flow levers, and how much contingent capital is desired for any purpose or as backup funding.

Tenor: whether to stagger maturities, how long to go out based on how long-lived the fixed assets or IP are.

Domestic vs. international, based on where the assets or cash flow are generated.

How attractive a target you want to be for acquirers; consider things like tenor and certain provisions that make it more expensive to terminate financing should you be acquired.

Straight debt vs. convertible, based on how ‘richly’ the company’s equity is being valued and your appetite to keep coupon payments low.

The debt/equity mix, which should consider things like the optimal weighted average cost of capital (WAAC), what peers are doing, etc.

“S&P has a good primer on leveraged finance that I go back to frequently.”

Peer answer 2: “I have never liked the word optimal because I don’t think there is a perfect debt/equity mix, and if there were, then it’s always changing with the markets and other factors. We all know that as the amount of debt is increased, this lowers our WACC unless we push the leverage too high, and the perceived risk causes debt and equity investors to push up the costs.

Rather than try to find an optimal level, which could imply adding debt even without having a specific use for it, we added debt for specific use cases like share repurchases and M&A. We went from having no debt and no credit ratings to having lots of debt and ratings by the three main agencies.

The limiting factor for us on how high to go has been a combination of 1) how comfortable we feel with free cash flow generation and the ability to efficiently move it around the world to service debt and 2) the approximate limits that the rating agencies allow in order to maintain our investment grade (IG) ratings.

While the difference in cost of funding for IG and high yield has been small in recent years, we feel it is important to maintain IG as we all know things can change quickly. Consider your plans for the debt and what kind of credit rating you would like to target.

Aside from those, there could be a strategic reason why you might choose a much lower amount of debt (keeping dry powder for the future) or going past your debt target for a strategic acquisition.

“We have a general capital allocation strategy that is fairly common: free cash flow is first used for strategic purposes like investing back in the business or M&A.

After that, the uses would be repaying debt if we are temporarily over-levered and maintaining our dividend. If there is free cash flow available after that, then we might consider stock repurchases unless there is a strategic reason to build cash.

We have a capital return policy that doesn’t specify how much we do but is more about how we go about it operationally—like open market versus use of 10b5-1 plans, etc.”

NeuGroup Insights reached out to Lucia Greenblatt, managing director of technology banking at MUFG, who agreed with the points made by members and added these:

“Optimal is a dynamic concept, underpinned by a company’s objectives, growth cycle and the economic environment. We’ve seen the perception of what’s optimal being tested throughout the pandemic, with the most emphasized elements being liquidity, cash flow generation and access to liquidity (markets being open at reasonable terms).

“In normal times, companies with large excess cash balances can be subject to shareholder activism if they are perceived as inefficient capital allocators, with the cash being a drag on valuation.

“In volatile times, liquidity becomes a strong asset that provides the flexibility to perform though the cycle without the need to raise capital at unfavorable terms; it enables the company to explore market opportunities such as buying assets in distress, or add inventory when supply chains are dislocated.

In stable times, the company can choose to return a portion of the excess cash to shareholders.

“In the software space, as companies continue to mature, they tend to keep a large cash balance as dry powder; when they tap capital markets, they tend to target a comfortable leverage ratio or a leverage-neutral balance sheet. When valuations dip, they can signal to the market that they are undervalued by announcing large share repurchase programs.”

More corporates are expanding the parts played by diversity firms beyond sharing deal economics with bigger banks.

Corporates committed to the long-term success of brokerage firms that are owned and run by Black and Hispanic people as well as women and veterans are going to greater lengths to give these so-called diversity firms not only fees, but more meaningful roles in capital markets transactions.

That key takeaway emerged at a late January meeting of the NeuGroup for Diversity and Inclusion working group. A panel of treasury professionals discussed how their relationships with diversity firms have evolved in the last few years and how they’re ensuring that big banks support their efforts.

The panelists also shared how they select diversity firms, which several members noted are growing in number as more corporates push to meet both D&I and ESG goals. We’ll explore the selection process in a future post.

More corporates are expanding the parts played by diversity firms beyond sharing deal economics with bigger banks.

Corporates committed to the long-term success of brokerage firms that are owned and run by Black and Hispanic people as well as women and veterans are going to greater lengths to give these so-called diversity firms not only fees, but more meaningful roles in capital markets transactions.

That key takeaway emerged at a late January meeting of the NeuGroup for Diversity and Inclusion working group. A panel of treasury professionals discussed how their relationships with diversity firms have evolved in the last few years and how they’re ensuring that big banks support their efforts.

The panelists also shared how they select diversity firms, which several members noted are growing in number as more corporates push to meet both D&I and ESG goals. We’ll explore the selection process in a future post.

Progression from passive to active. In addition to increasing the number of diversity firms participating in their most recent transactions, each panelist said the role played by the firms has become more meaningful than in past deals where a relatively small number of diversity firms played passive or small parts, largely consisting of receiving fees.

“Early on, we were solely utilizing the diversity space as book managers in a passive role,” one panelist said. “Over the last year or so, we’ve transitioned in a rather big way and started to utilize diversity firms as joint leads on our US dollar transactions.

“Not only does the diversity firm get to enjoy the same access and economics, but it really enables them to develop their story, create contacts with the other lead book runners, get exposed to the process and enhance their relationship with larger, tier-one investors.”

One NeuGroup member who had been using two or three diversity firms in debt deals and giving them economics but no more, expanded to eight in a recent debt offering.

The other, more significant change: “I asked [the diversity firms] to give me their orders because I wanted to really demonstrate that this was meaningful to us,” they said. “So I personally got their orders summarized. I sent them to the diversity coordinator so that individual knew that I was paying attention.”

Before the final pricing of the deal, this member took extra time to review the allocation of bonds by tenor and diversity firm with the D&I coordinator. “As a result, the eight firms got equal allocation to all the other banks.”

Managing big banks. Indeed, corporates leading the push for a more level playing field for diversity firms to compete with bulge bracket banks have to be prepared to take a hands-on approach to the allocation of their deals. In cases like the one above, it may involve close coordination with a D&I coordinator, usually one of the lead managers whose role is to support the diversity firms.

One treasurer said he lost sleep over the allocation process in the past because some banks would say one thing and do another. “It does get hard, but we don’t leave it to the banks anymore,” he said. “We actually mandate to the banks what the diversity firms are going to get.

“It’s not going to be, ‘we’ll just give them the economics but we won’t give them the paper.’ And that’s usually what happened in the old days. But it’s not happening today because a lot more of us have a lot more experience with it and know exactly what’s happening.”

Another panelist sees progress in how big banks work with diversity firms. “It’s been an evolution. The bulge bracket firms have taken more of an interest in enhancing and mentoring the diversity firms,” he said. “It’s become more supportive, more of a mentor relationship.

“And we take a lot of time thinking about who we are going to pair a diversity firm with. We try to pair them with firms with a rather large presence in the market, firms we’re comfortable with, firms that have proven to be good partners in the diversity space.”

Miles to go. None of the panelists expressed satisfaction with where their companies stand on the road to enhancing the role and stature of brokers owned by minorities, women and vets. They all want their organizations to make more progress, while acknowledging that some corporates are farther along than others on this path.

“We all do things a little differently,” one member said about the group of panelists. “And it’s really a matter of where you are in your evolution and where you want to do more. But we’re all about how do we continue to evolve this, make it more meaningful and more inclusive.”

“I’m going to do something completely different in the future,” one treasurer said. “I want to change the way we do things, where we don’t have much reliance on the banks anymore. The diversity firms are getting so much better, with the talent that they’re bringing in and the bandwidth that they have now. So we’re going to narrow it down to fewer banks, more diversity firms. And you’re starting to see more and more corporates doing this.”

Members at a special NeuGroup session discuss banks, dividends, SWIFT payments and more amid Russia-Ukraine tensions.

Cross-border payments with SWIFT, relationships with local and foreign banks and repatriating funds are among the key focal points of corporate treasury teams planning for possible US and EU sanctions if Russia attacks Ukraine. That takeaway surfaced Wednesday at a NeuGroup session on contingency planning attended by more than 80 members—a packed virtual house that shows the significance of the situation for corporates with business and staff in Russia.

The session was led by NeuGroup’s Scott Flieger, director of peer groups, and Paul Dalle Molle, senior executive advisor and a former international banker. Mr. Dalle Molle observed, “Mostly, people are wondering how to improve what they are already doing and how to prepare for changes to SWIFT or other funds transfer regimes if sanctions bite hard. Very few are looking at massive repatriations because of this crisis; it’s too late for that.”

He noted that all the members at the session have some experience dealing with sanctions in Russia and elsewhere, and will all fully comply with US and European laws. That said, as long as corporates are allowed to operate in a country, they need to find the best sanctions-compliant ways to continue their business operations.

Members at a special NeuGroup session discuss banks, dividends, SWIFT payments and more amid Russia-Ukraine tensions.

Cross-border payments with SWIFT, relationships with local and foreign banks and repatriating funds are among the key focal points of corporate treasury teams planning for possible US and EU sanctions if Russia attacks Ukraine. That takeaway surfaced Wednesday at a NeuGroup session on contingency planning attended by more than 80 members—a packed virtual house that shows the significance of the situation for corporates with business and staff in Russia.

The session was led by NeuGroup’s Scott Flieger, director of peer groups, and Paul Dalle Molle, senior executive advisor and a former international banker. Mr. Dalle Molle observed, “Mostly, people are wondering how to improve what they are already doing and how to prepare for changes to SWIFT or other funds transfer regimes if sanctions bite hard. Very few are looking at massive repatriations because of this crisis; it’s too late for that.”

He noted that all the members at the session have some experience dealing with sanctions in Russia and elsewhere, and will all fully comply with US and European laws. That said, as long as corporates are allowed to operate in a country, they need to find the best sanctions-compliant ways to continue their business operations.

Dividends. Repatriating money from Russia through dividends generated considerable discussion, much concerning how long it takes, even in the best of times. Members said it ranges from three to 11 months to organize and pay dividends, although one treasurer is on the verge of accomplishing it in just six weeks. His company has retained earnings from its last fiscal year that are available to dividend and doesn’t have to wait for the official closing of the 2021 books.

Documentation and the relative complexity or simplicity of a corporate’s legal entity structure seem to be the two biggest issues that delay the process, Mr. Dalle Molle noted.

Another member said his company had not made dividends from Russia a priority following an entity restructuring because the business wasn’t generating significant cash there at the time. But that changed in the last year as its business grew. He called that bad timing in terms of prioritizing the movement of retained earnings out of Russia. “But it’s a priority now, I can tell you that,” he said.

Banks. Mr. Dalle Molle, who has been talking to corporates for weeks about Russia, said some members believe that having a mix of indigenous and international banks provides a natural hedge against the risk of restrictions, sanctions or counter sanctions that could affect foreign banks differently than local institutions. At this point, though, members are not rushing to open new accounts at local banks.

Citibank was by far the name most frequently mentioned by members as their main local bank in Russia. Other banks named often included Rosbank (SocGen) and Unicredit. Deutsche Bank, MUFG, Credit Agricole, BNP, JP Morgan and VTB were also mentioned. There was some speculation that a large Asian bank like MUFG might have more flexibility than a US or European bank in the event of sanctions.

Some members are discussing with international banks whether funds held by their Russian subsidiaries in the Moscow branches of those banks would be affected by sanctions differently than deposits held in, say, the London branch of the same bank.

SWIFT and payments. Some news reports indicate that the likelihood of sanctions including a SWIFT cutoff is receding, in part because it may do more harm to Western interests than damage to Russia, Mr. Dalle Molle noted. But some companies at the meeting mentioned exploring the option of making prepayments for their businesses just in case the situation worsens.

If a SWIFT alternative is needed, the most likely channel seems to be the Chinese Cross-Border Inter-Bank Payments System (CIPS). It’s a very small system compared to SWIFT, but it works, and 13 Russian banks are already members.

In addition, Mr. Dalle Molle said, a digital ruble is currently being tested in Crimea, but that won’t likely be a viable alternative for several more years.

A “mini-SWIFT” for humanitarian payments called INSTEX that’s sponsored by the EU could potentially be used by life science companies and other corporates with cross-border humanitarian goods and services.

For domestic payments and the use of cards, the consensus is that the Russian payments clearing system SPFS and the domestic Russian card system “Mir” (NPCS) will work well during sanctions and that companies can use these for most of their local payment, local currency needs with customers, suppliers and staff.

Contingency planning. Mr. Dalle Molle said multinational companies have been derisking in Russia for a decade, even as they expand their business there. But the heightened risk of sanctions or other business interruptions means it’s worth reminding corporates doing business there to have contingency plans for:

A new NeuGroup survey reveals that treasurers are focused on driving company growth.

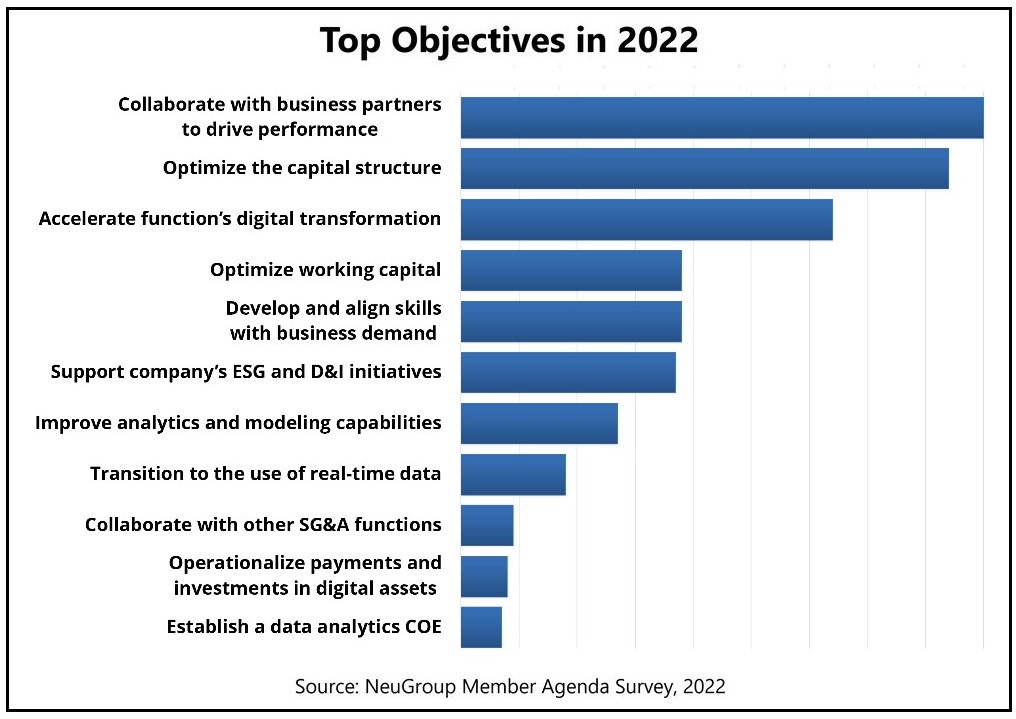

Treasurers at the world’s leading companies are doubling down on their commitments to expand beyond traditional areas like liquidity management and spend more time in strategic zones. That’s among the key takeaways from the January 2022 NeuGroup Members Agenda Survey. In it, respondents picked their top three objectives from a list of 11. Their answers, shown in the chart above, reveal an emphasis on driving better enterprise financial performance.

A new NeuGroup survey reveals that treasurers are focused on driving company growth.

Treasurers at the world’s leading companies are doubling down on their commitments to expand beyond traditional areas like liquidity management and spend more time in strategic zones. That’s among the key takeaways from the January 2022 NeuGroup Members Agenda Survey. In it, respondents picked their top three objectives from a list of 11. Their answers, shown in the chart above, reveal an emphasis on driving better enterprise financial performance.

By collaborating with business partners (No. 1) and optimizing capital structure (No. 2), treasury can provide companies with support for decision-making and financing required to increase revenue and manage risk.

In addition, by selecting digital transformation as their No. 3 priority, treasurers aim to reduce process cost and life cycle, freeing up staff capacity to focus on strategic tasks. (Some headline-grabbing topics such as real-time data and crypto got much lower scores.)

However, the realization of treasurers’ top priorities depends on other factors, which are getting less attention, according to the survey. For example, improved analytics and modeling capabilities are crucial to treasury’s ability to contribute business value through better decision support, but ranked at No. 7.

Strategic advisement must also include collaboration with other parts of finance, such as FP&A. But treasurers rated its importance at No. 9.

NeuGroup Insights will bring you more takeaways and analysis of the survey results in the weeks to come.

Former NeuGroup Tech20 member Eric Ball describes his transition from treasurer to VC investor and more in our debut podcast.

Welcome to the inaugural edition of the NeuGroup Insights Podcast! We kick things off with former Oracle treasurer and Tech20 member Eric Ball, a longtime NeuGroup friend who is now general partner and co-founder of Impact Venture Capital—just one of numerous hats he wears. He’s also co-founder and chairman of capital markets startup CapConnect+, chairman of the special purpose acquisition company Archimides Tech SPAC Partners and a board advisor to Kyriba.

Former NeuGroup Tech20 member Eric Ball describes his transition from treasurer to VC investor and more in our debut podcast.

Welcome to the inaugural edition of the NeuGroup Insights Podcast! We kick things off with former Oracle treasurer and Tech20 member Eric Ball, a longtime NeuGroup friend who is now general partner and co-founder of Impact Venture Capital—just one of numerous hats he wears. He’s also co-founder and chairman of capital markets startup CapConnect+, chairman of the special purpose acquisition company Archimides Tech SPAC Partners and a board advisor to Kyriba.

In his interview with NeuGroup senior director Anne Friberg, Eric shares a range of insights about treasury technology, fintechs he’s investing in and watching, and how treasury skills have paid off in evaluating fintechs in the treasury and Office of the CFO space.

“When I transitioned from a treasury role to a startup CFO role and then to venture, those analytical skills that one gets in treasury were certainly relevant,” he said. “I would say that venture investing requires a blend of art and science, and treasury helps with both,” he tells Anne.

Hear all of Eric’s insights—including how being a member of NeuGroup helped him—in the full podcast.

As more pension plans enjoy surpluses, they consider derisking strategies including hibernation vs. termination.

Participants at a recent meeting of NeuGroup for Pensions and Benefits sponsored by Insight Investment voiced concerns about pursuing buyouts of their pension plans by insurers and leaned more toward hibernating plans, although they left room for exceptions.

Participants at a recent meeting of NeuGroup for Pensions and Benefits sponsored by Insight Investment voiced concerns about pursuing buyouts of their pension plans by insurers and leaned more toward hibernating plans, although they left room for exceptions.

Hibernation occurs with so-called frozen plans that are no longer accruing future benefits and are usually well-funded or overfunded. It involves managing risk to reduce volatility by adopting a liability-driven investment strategy and letting the payout of benefits shrink the plan.

Buyouts are still an option, and participants acknowledged selling pieces of their plan liabilities and finding reasonable prices. In particular, selling low-balance participant liabilities can have straightforward economic benefits because an insurance company, unlike a corporate, is not charged PBGC fees for pension liabilities.

The rising funded status of corporate pensions has made both hibernation and plan terminations more feasible. And pension funding will likely remain strong as the positive impact of rising interest rates partially offsets recent sell-offs in stocks and other equity-like investments.

As more pension plans enjoy surpluses, they consider derisking strategies including hibernation vs. termination.

Participants at a recent meeting of NeuGroup for Pensions and Benefits sponsored by Insight Investment voiced concerns about pursuing buyouts of their pension plans by insurers and leaned more toward hibernating plans, although they left room for exceptions.

Hibernation occurs with so-called frozen plans that are no longer accruing future benefits and are usually well-funded or overfunded. It involves managing risk to reduce volatility by adopting a liability-driven investment strategy and letting the payout of benefits shrink the plan.

Buyouts are still an option, and participants acknowledged selling pieces of their plan liabilities and finding reasonable prices. In particular, selling low-balance participant liabilities can have straightforward economic benefits because an insurance company, unlike a corporate, is not charged PBGC fees for pension liabilities.

The rising funded status of corporate pensions has made both hibernation and plan terminations more feasible. And pension funding will likely remain strong as the positive impact of rising interest rates partially offsets recent sell-offs in stocks and other equity-like investments.

Split objectives. Sweta Vaidya, head of LDI Solution Design at Insight Investment, said that as plans approach and exceed fully funded status, the firm’s clients have differing end-state objectives.

Some intend to continue selling parts of their pension liabilities and taking risk off their books, pursuing a full plan termination eventually.

Others want to keep their plan open for employees and manage the risk going forward, targeting funding of 110% to 120% to account for future service costs and minimize cash contributions and volatility in the income statement.

One member said that under hibernation, the rigid and costly asset-liability matching of insurance companies can be avoided while still organizing assets to provide liquidity for upcoming benefit payments. “So we do a kind of cash flow matching on coupon payments,” he said.

Buyout concerns. Defined benefit plan participants may not be happy when their pension is involuntarily transferred to an insurance company and the company is no longer on the hook. And there can be indirect costs.

A participant said his company’s defined benefit and 401(k) plans share the same manager and other retirement plan-related service providers, so selling off the former could end up raising fees on the latter and also impact revolving credit availability from the financial institution.

That said, one member said his team has looked at selling a portion of the company’s plan over the last few years and executed a buyout piece earlier in 2021. Pricing was favorable—not below the accounting value of the liability, but “less than we’ve seen in the past and better than expected,” he said.

However, Ms. Vaidya at Insight notes that selling off the most attractive and least costly portions of a pension liability means a company is holding riskier, more difficult-to-manage liabilities. Those may have been naturally hedged previously by the liabilities the corporate sold.

Surplus benefits. Companies sponsoring pensions pay significant financial penalties if they return surpluses accrued under the hibernation strategy to the corporation. Instead, the corporate may be able to:

Transfer money to other post-employment benefit plans, such as health and life insurance, as permitted under Section 420 of the US tax code, albeit with some residual penalties.

Apply surpluses to other employee benefits such as 401(k) matches—a possible alternative to wage increases.

Fund other sponsored pensions, such as those taken on as part of an acquisition.

Balancing efficiency and value, and managing people vs. technology, will be key priorities for finance in the future.

By Joseph Neu

Providing foresight on the future of treasury is always a crowd-pleaser with NeuGroup members. During sessions over the last few months, I had the privilege of sharing my current thoughts on the topic and hearing member reactions.

A shared passion project. Most of these sessions (and more may be coming) have been done in partnership with Jean Furter, now treasurer of Poly, who has also made delivering insight on treasury’s future a passion project. We shared some of Jean’s views in a NeuGroup Insights post last month.

Balancing efficiency and value, and managing people vs. technology, will be key priorities for finance in the future.

By Joseph Neu

Providing foresight on the future of treasury is always a crowd-pleaser with NeuGroup members. During sessions over the last few months, I had the privilege of sharing my current thoughts on the topic and hearing member reactions.

A shared passion project. Most of these sessions (and more may be coming) have been done in partnership with Jean Furter, now treasurer of Poly, who has also made delivering insight on treasury’s future a passion project. We shared some of Jean’s views in a NeuGroup Insights post last month.

Here are my five key thoughts:

Scale by balancing maximum efficiency and value creation. One vision of the future I heard holds that treasurers setting goals will need to choose between maximizing efficiency or value. But Jean helped me understand the future will be built on the interplay between efficiency and value, rather than one or the other: The more efficient treasury is, the more bandwidth it has for value-adding activities, including supporting an enterprise as it scales into the future. Indeed, the current focus of inefficient finance teams should be almost entirely on building efficiency, so they are in the best position to maximize added value in the future. The desired end state is treasury distinguishing itself as a value maximizer; that’s the future we want.

Envision financial plumbing as end-to-end, and embed it. Finance operations in the future will tear down silos creating friction that plagues order-to-cash or procure-to-pay processes and the people who run them. Future-oriented treasuries will help their firms model cash flowing into and out of the enterprise and align finance (not just treasury) operations to them. More importantly, they will take the next step to digitalization and embed the inflow and outflow processing into the business product or service—all with a positive contribution to the user experience and interface at the front end, and efficiency for the digital back office. This links treasury with profit and profit from the business in a way that is also part of the future we want.